[[{“value”:”

By Wolf Richter for WOLF STREET.

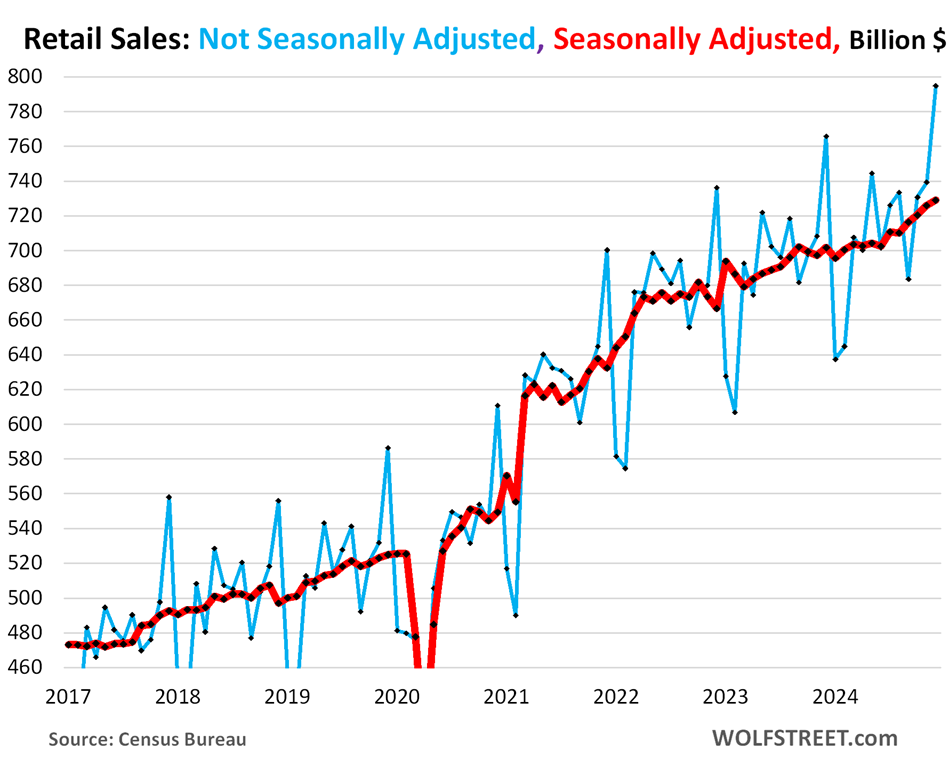

Retail sales rose by 0.45% in December from November (+5.5% annualized), and November and October were revised higher – October from +0.46% to +0.56%, and November from +0.69% to +0.77% – and it’s on top of these upwardly revised sales that December sales grew by another 0.45%, all seasonally adjusted.

The slow first half was followed by a blistering acceleration in the second half, particularly over the past four months.

Not seasonally adjusted, December sales rose to a record of $794 billion. Ecommerce was a big winner; sales jumped 10.2% year-over-year to $156 billion, for a share of 19.6% of total retail sales, surpassing auto dealers and making it the #1 retailer category for the month.

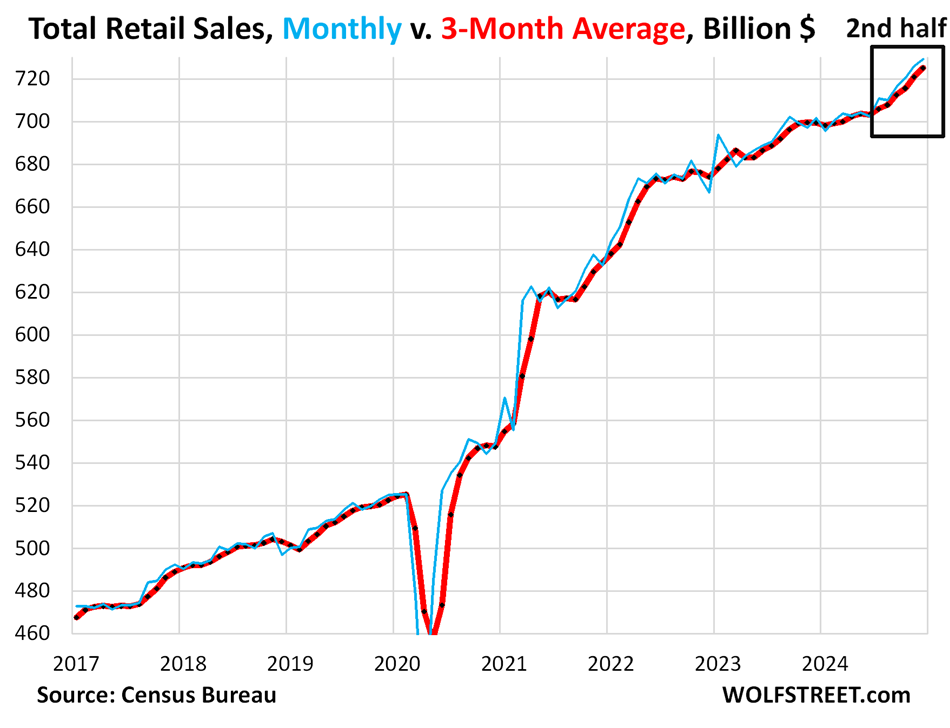

The acceleration in the second half: Someone turned on the spigot.

The three-month average – which includes the prior revisions, irons out the month-to-month squiggles, and shows the trend better – rose by 0.59% in December, seasonally adjusted, after three-month average growth rates of +0.74% in November, +0.45% in October, and +0.66% in September.

To get a point of reference, on an annualized basis, December’s three-month average growth rate of 0.59% amounts to an annual rate of 7.3%. November’s growth rate of 0.74% amounts to an annual rate of 9.3%. That is huge growth for the US.

Someone turned on the spigot in the second half, and retail sales gushed, after a slow first half. June had been handicapped by the CDK hack of the cloud-based dealership software of thousands of dealers that prevented them from processing sales in June, which then got processed in July, shifting that portion of retail sales from June to July, but that doesn’t explain the surge in retail sales over the past four months of 8.2% annualized:

- 6 months January-June total: +0.1%, annual pace +0.2%.

- 6 months July-December total: +3.8%, annual pace +7.7%.

- 4 months September-December total: +2.67%, annual pace +8.2%.

Note the steepening of the slope over the past six months (black box):

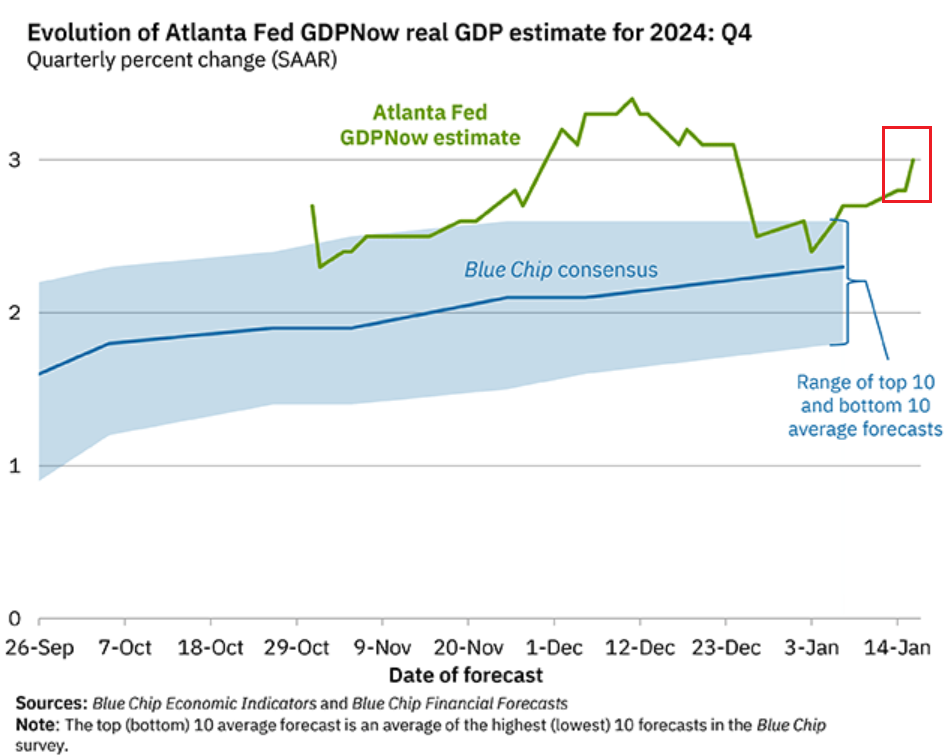

GDPNow jumped to 3.0% due to these retail sales.

The Atlanta Fed’s GDPNow “nowcast” for Q4 “real” GDP (inflation adjusted) jumped to a growth rate of 3.0% today, upon inclusion of the retail sales data.

Over the past 15 years, the US has averaged about 2% “real” GDP growth. If GDPNow is on target, Q4 real GDP would come in at about 3.0%. Over the past five quarters, there was only one weakling, Q1 2024 with 1.6% inflation-adjusted growth. The other four quarters ranged from 3.0% to 4.4% inflation-adjusted growth, which is huge for the US.

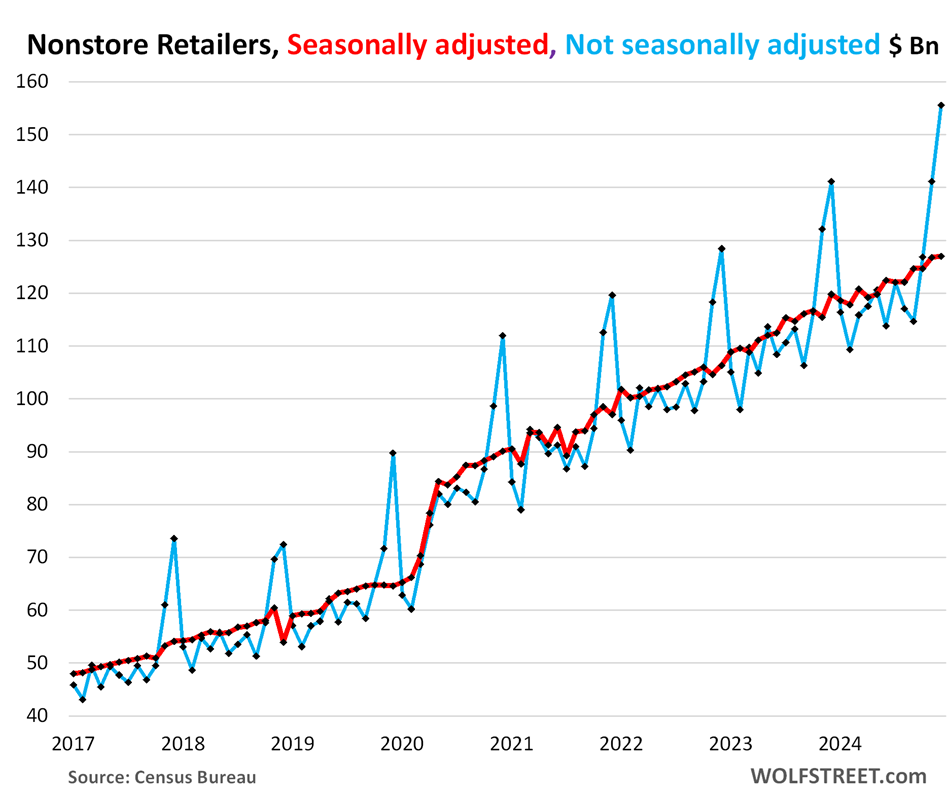

Ecommerce and other “nonstore retailers” (ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets): Total sales not seasonally adjusted jumped by 10.2% year-over-year to $156 billion (blue). Huge seasonal adjustments reduced that to $127 billion (red). The three-month average sales in December from November, seasonally adjusted, jumped by 0.62%:

More consumers, more workers, more jobs, more money.

Our Drunken Sailors, as we lovingly and facetiously have come to call them, are in the mood to spend. The labor market has been solid, with an additional 2.23 million payroll jobs created in 2024, and with hourly earnings up by 4%, outpacing inflation for the second year. Consumers are sitting on vast and ballooning piles of cash in money-market funds and CDs. Stocks, home prices, and cryptos have soared in recent years, and consumers that hold them (64% are homeowners and many hold stocks in their retirement funds) are feeling flush.

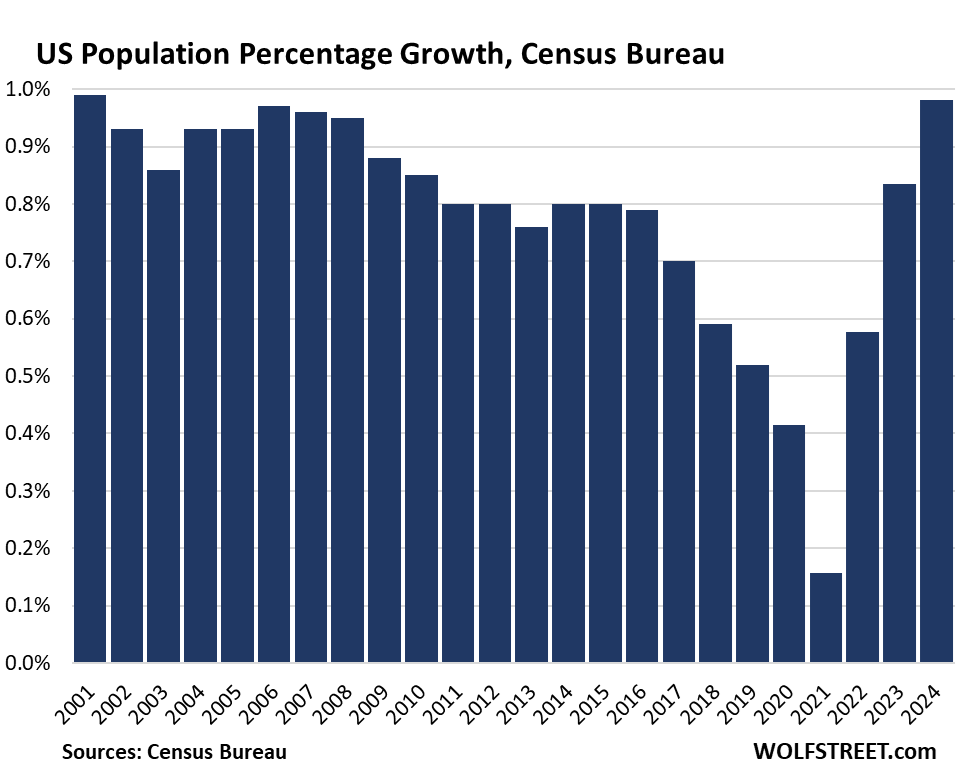

And there are a lot more consumers: net immigration added 2.8 million people to the population in the 12 months through July 2024, and 4.0 million over the prior two months, and so the population of the US over those three years soared by 2.4%, including by nearly 1% over the 12 months through July, the biggest percentage growth rate since 2001, according to the population updates by the Census Bureau in December.

Many of these new arrivals are already working, and they’re spending money too (detailed discussion here):

Amid this strong demand, inflation catches its second wind. The Fed needs to watch out.

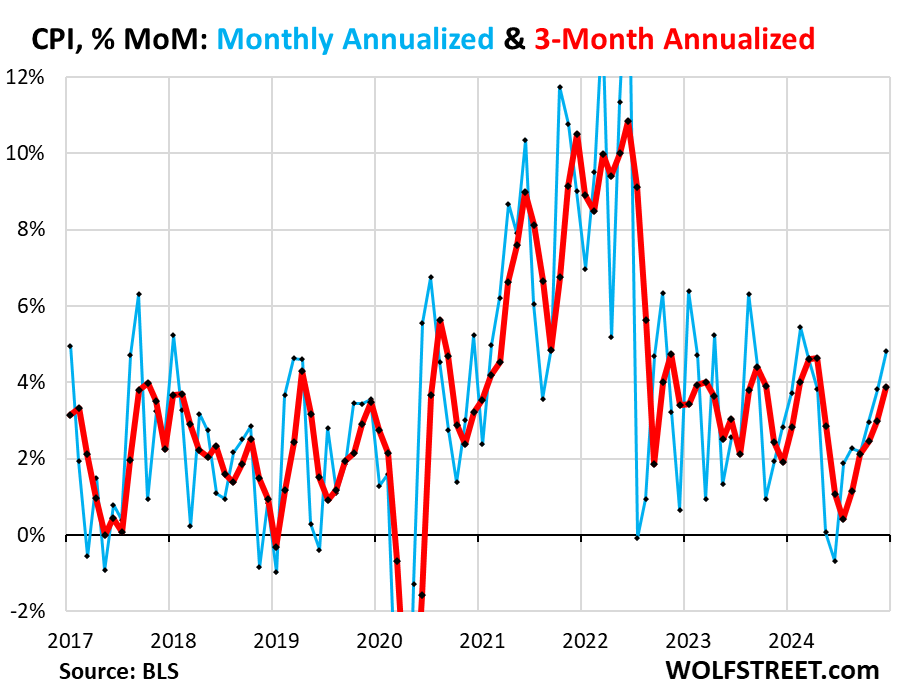

Inflation has been accelerating for the past few months. The latest piece of that puzzle came yesterday: The Consumer Price Index rose by 0.39% (+4.8% annualized) in December from November, the sharpest increase since February 2024. It has been accelerating since the low point in June (blue).

The three-month CPI, which irons out some of the month-to-month squiggles, jumped by 3.9% annualized, the sharpest increase since April, and the fifth month-to-month acceleration in a row.

This acceleration of the month-to-month CPI inflation rate over the past four months parallels the surge in retail sales.

The year-over-year CPI rose by 2.9%, the sharpest increase since July, and the third month in a row of acceleration (detailed discussion here).

But our drunken sailors are not dropping money everywhere equally.

Sales at nonstore retailers (mostly ecommerce) and at auto and parts dealers accounted for nearly 40% of total retail sales in December.

Some of the other major categories also booked strong sales, but not all. Some of the unique pandemic booms, such as home improvements, have blown over and aren’t coming back, it seems.

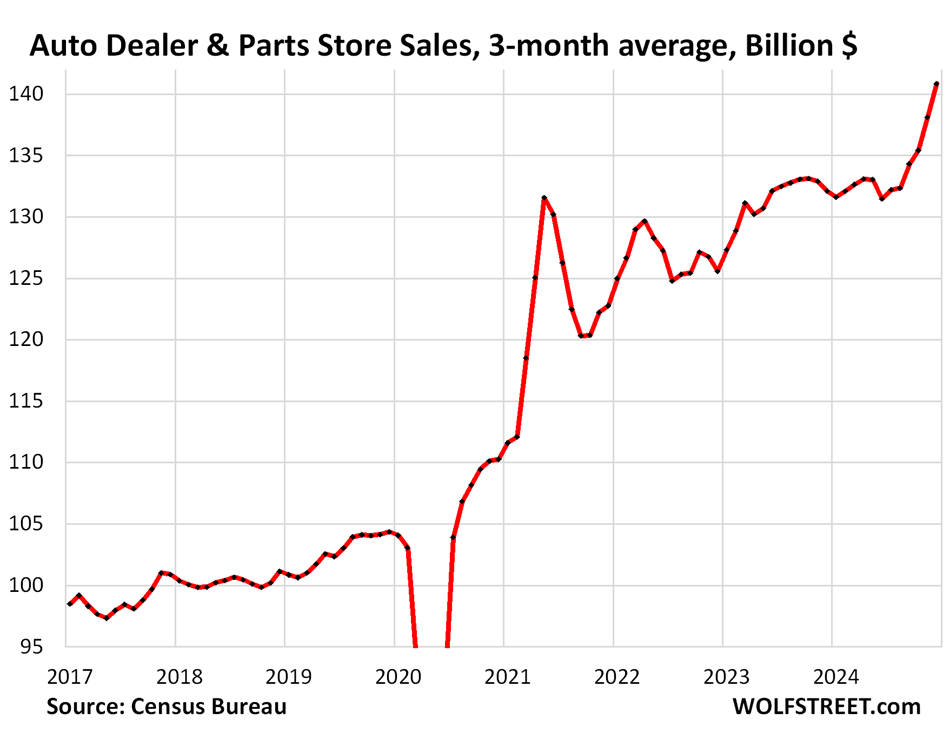

New and used vehicle dealers and parts stores, the second largest category in December: Sales on a three-month average basis soared by nearly 2% (seasonally adjusted) in December from November, and by 7.5% year-over-year (not seasonally adjusted) to $141 billion. This was a very strong finish of a year that had started out somewhat slow-ish.

The spike in dollar-sales of new and used vehicles in 2021 and 2022 was caused by ridiculous price increases in used vehicles and by a combination of addendum stickers, lack of incentives, and higher MSRPs in new vehicles, amid the shortages at the time. Starting in mid-2022, used vehicle prices began to plunge, and new vehicle prices flattened out, and though unit sales increased, dollar sales flattened out.

But over the past few months, new and used vehicle prices have started rising again, which contributed to the worst month-over-month CPI inflation reading since February and the worst year-over-year inflation reading since July, as we discussed here yesterday. These price declines caused the dollar-sales for those 18 months to flatten out, despite rising retail unit-sales.

This recent rise in new and used vehicle prices and the strong volume sales created this spike in dollar sales at new and used vehicle dealers.

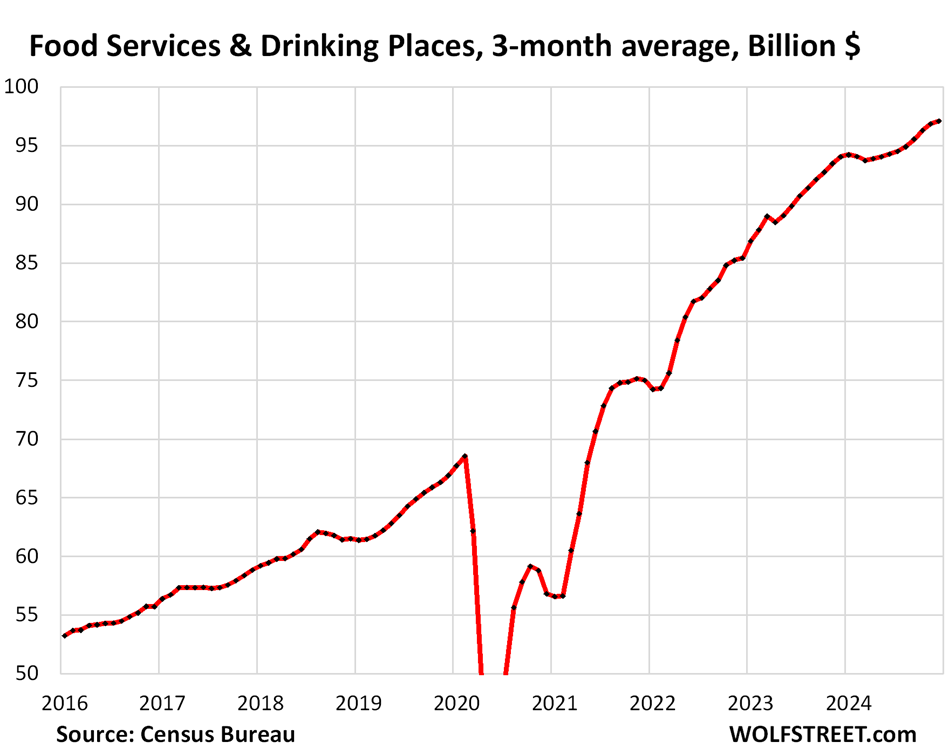

Food services and drinking places (#3 category, 13% of total retail), includes everything from cafeterias to restaurants and bars. After a decline in early 2024, moderate growth resumed:

- Sales: $97 billion

- From prior month, 3-month average: +0.23%

- Year-over-year: +3.2%

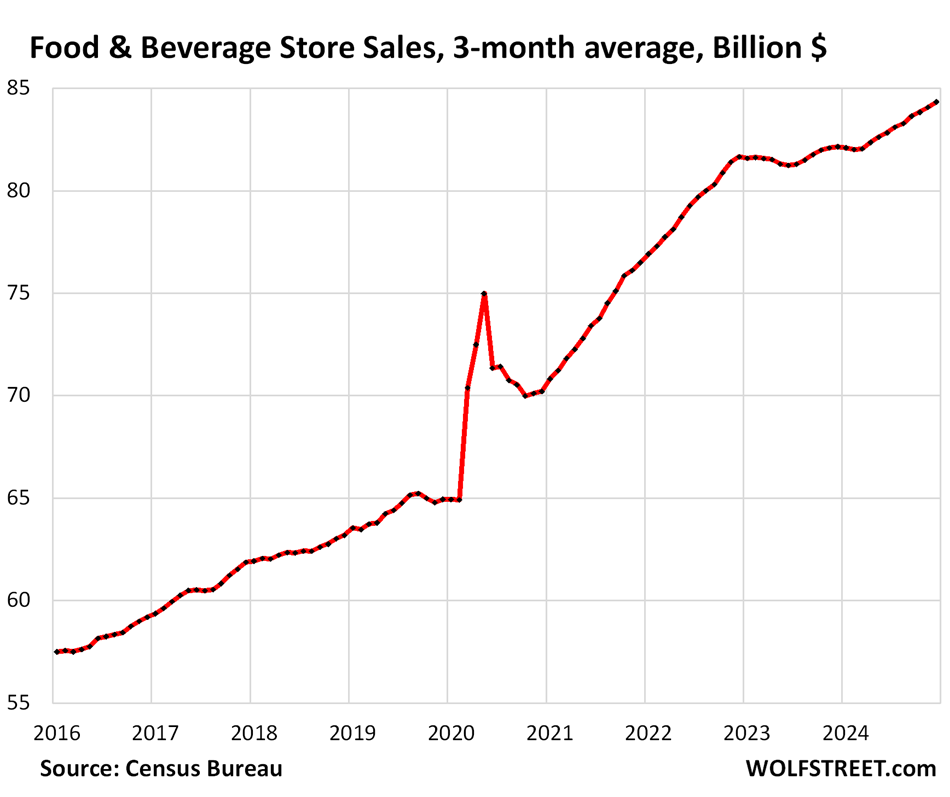

Food and Beverage Stores (12% of total retail). Prices per CPI for food at home exploded from 2020 to early 2023, which caused the spike in sales, then flattened out at high levels for a while, before starting to rise again:

- Sales: $85 billion

- From prior month, 3-month average: +0.30%

- Year-over-year: +2.7%

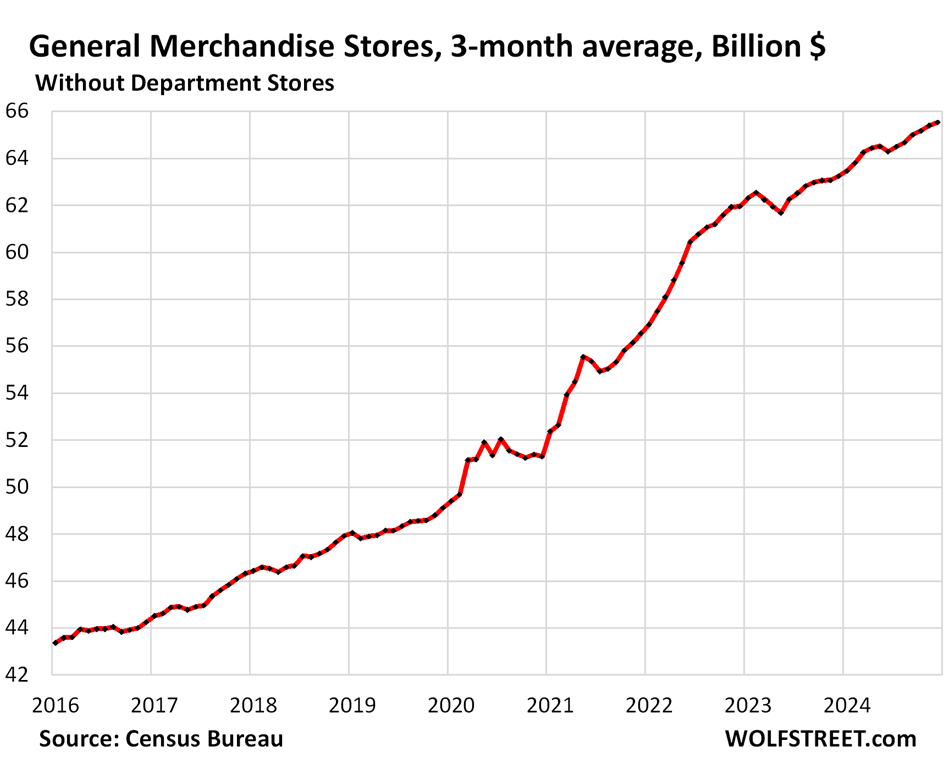

General merchandise stores, minus department stores (9% of total retail), including retailers such as Walmart, which is also the largest grocer in the US.

- Sales: $66 billion

- From prior month, 3-month average: +0.21%

- Year-over-year: +3.6%

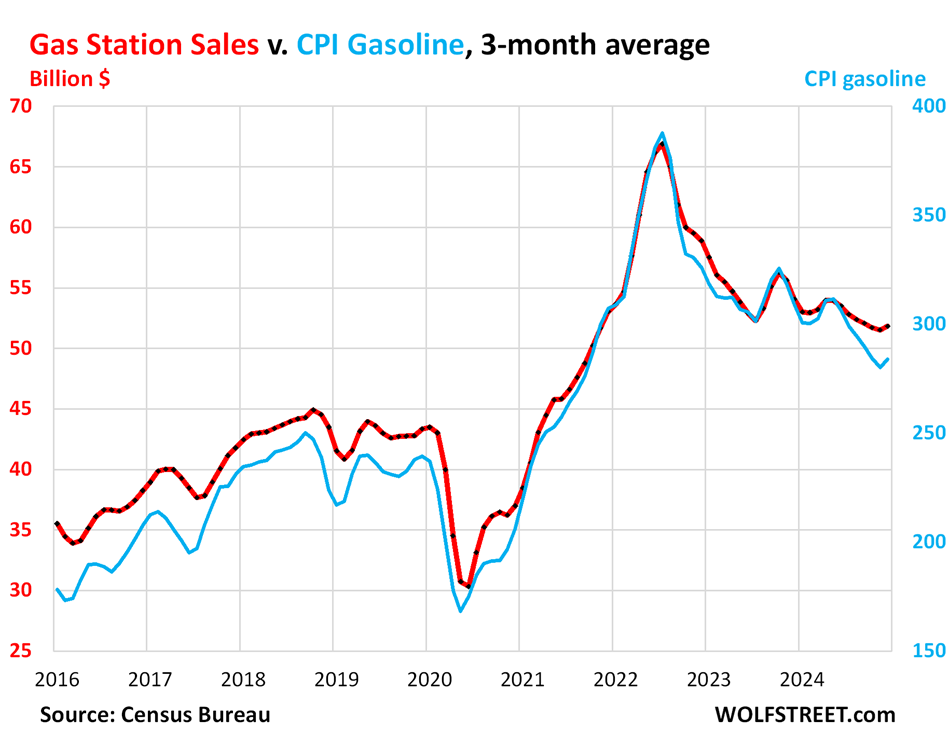

Gas stations (7% of total retail sales). Dollar-sales at gas stations move in near-lockstep with the price of gasoline. The price of gasoline started dropping in mid-2022 and continued to wobble lower until recently. These price declines pushed down dollar-sales at gas stations. Sales at gas stations also include all the other merchandise gas stations sell.

Gasoline prices started rising again recently, and so there’s this little hook for December, a three-month average that includes the price drop in October, a small rise in November, and the bigger rise in December:

- Sales: $52 billion

- From prior month, 3-month average: +0.63%

- Year-over-year: -4.1%

Sales in billions of dollars at gas stations (red, left axis); and the CPI for gasoline (blue, right axis):

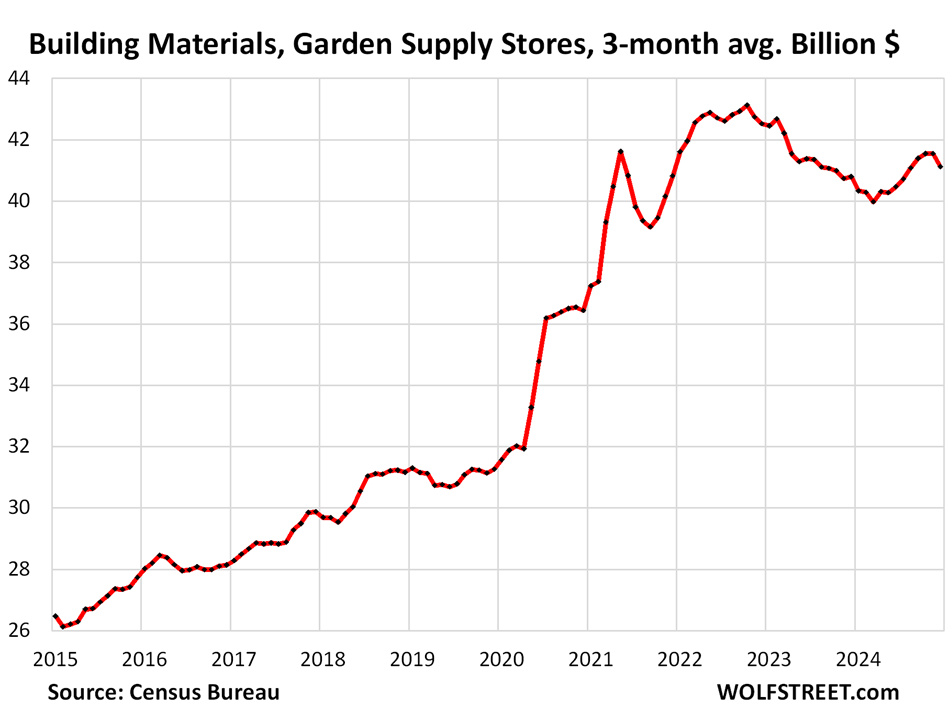

Building materials, garden supply and equipment stores (6% of total retail). The enormous remodeling boom during the pandemic fizzled in late 2022, and sales fell for a while. In 2024, sales started rising again from still very high levels, but late in 2024, they fizzled again:

- Sales: $41 billion

- From prior month, 3-month average: -1.0%

- Year-over-year: +0.8%

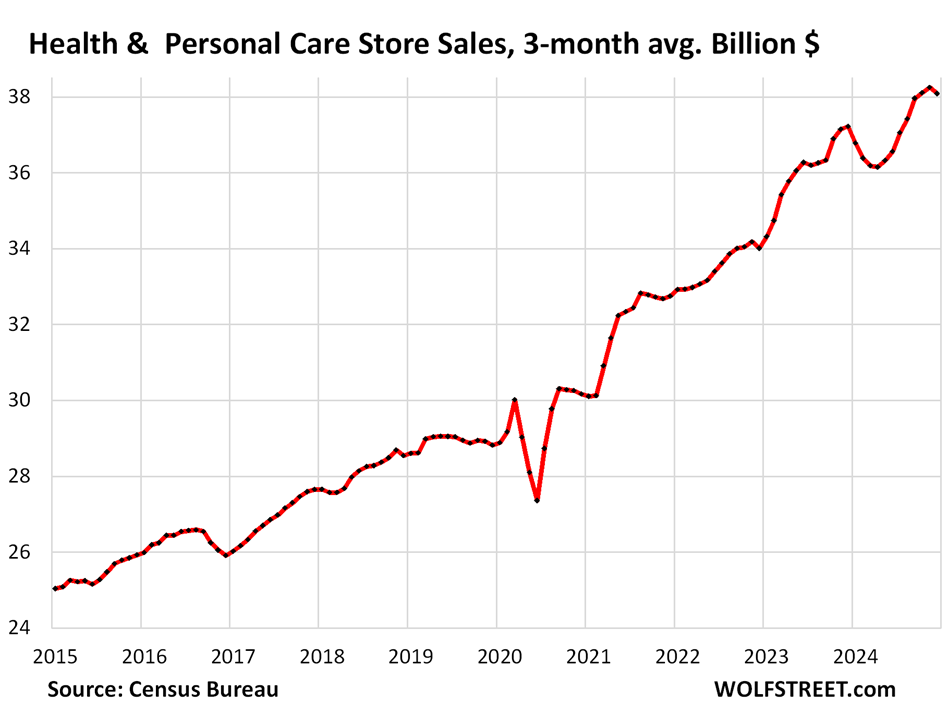

Health and personal care stores (5% of total retail:

- Sales: $38 billion

- From prior month, 3-month average: -0.42%

- Year-over-year: +2.3%

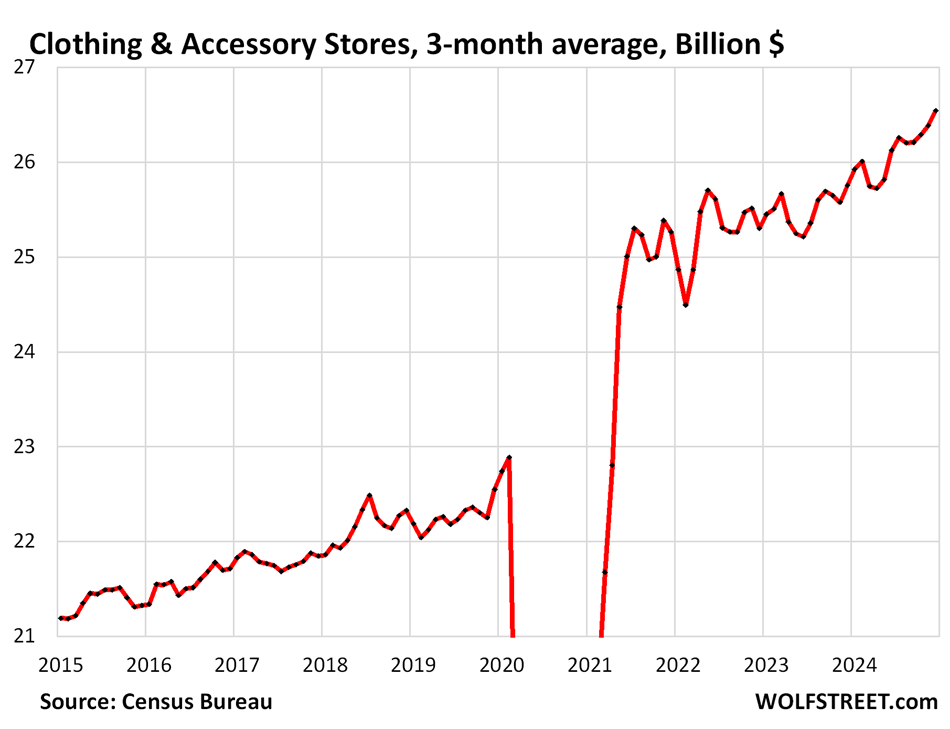

Clothing and accessory stores (3.7% of retail):

- Sales: $27 billion

- From prior month, 3-month average: +0.60%

- Year-over-year: +3.1%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post The Fed Needs to Watch Out: Amid Strong Demand from our Drunken Sailors, Retail Sales Surged in Late 2024 and Inflation Caught its Second Wind appeared first on Energy News Beat.

“}]]