[[{“value”:”

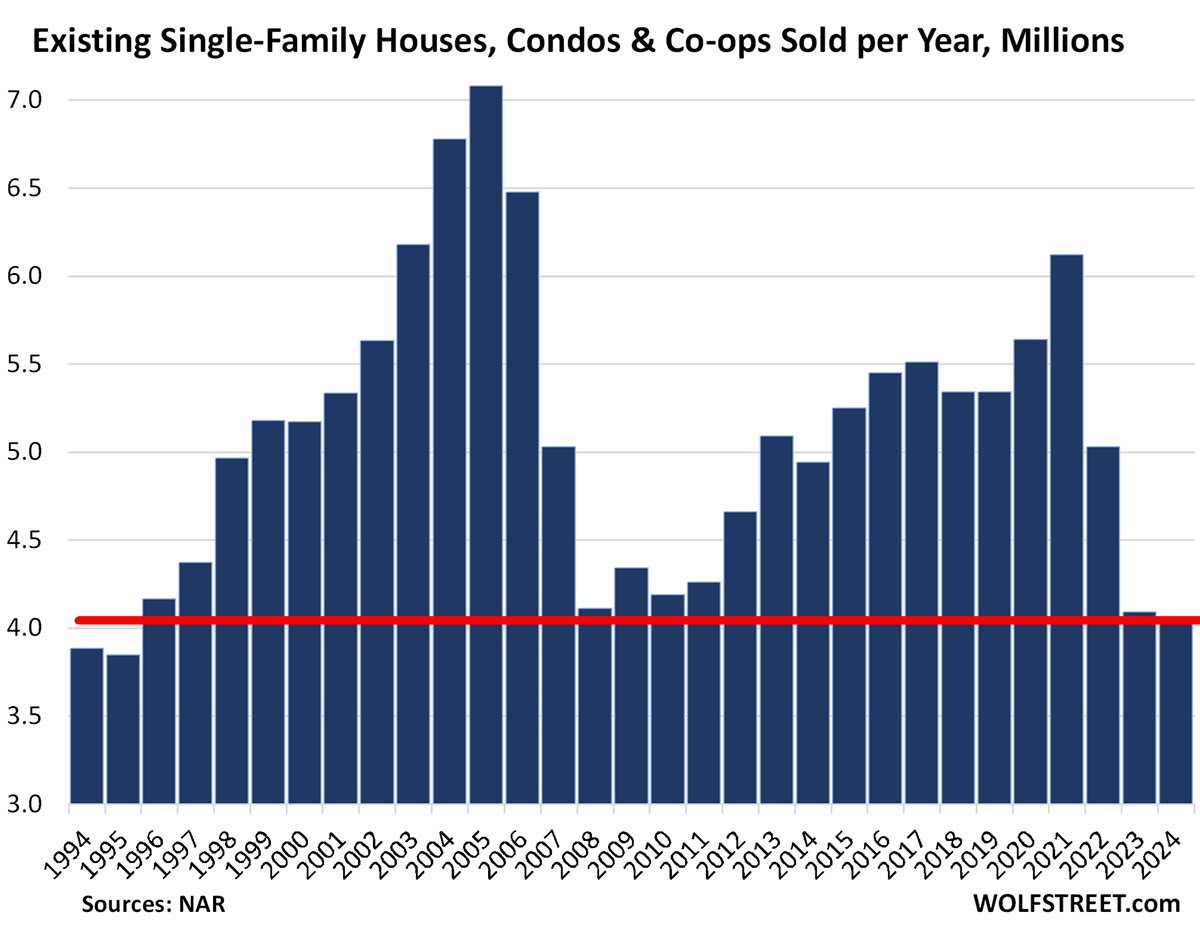

2024 was the worst year since 1995 for sales because prices are too high after the 50% spike in 2019-2022.

By Wolf Richter for WOLF STREET.

The market for resale homes has started to thaw just a little from its frozen condition as more buyers and sellers started getting used to the 7% mortgage rates, rather than waiting for them to plunge or whatever. And more “locked-in” homeowners are selling their homes to deal with changes in life, thereby giving up their below-4% mortgages. So sales volume ticked up a little over the past few months from the deep-freeze levels before, but remained still very low.

Sales of existing single-family houses, townhouses, condos, and co-ops that closed in December rose to 329,000 homes, not seasonally adjusted, up by 10.8% from December 2023, but still down by 36% from December 2021, testimony to the ongoing but slightly softening demand destruction.

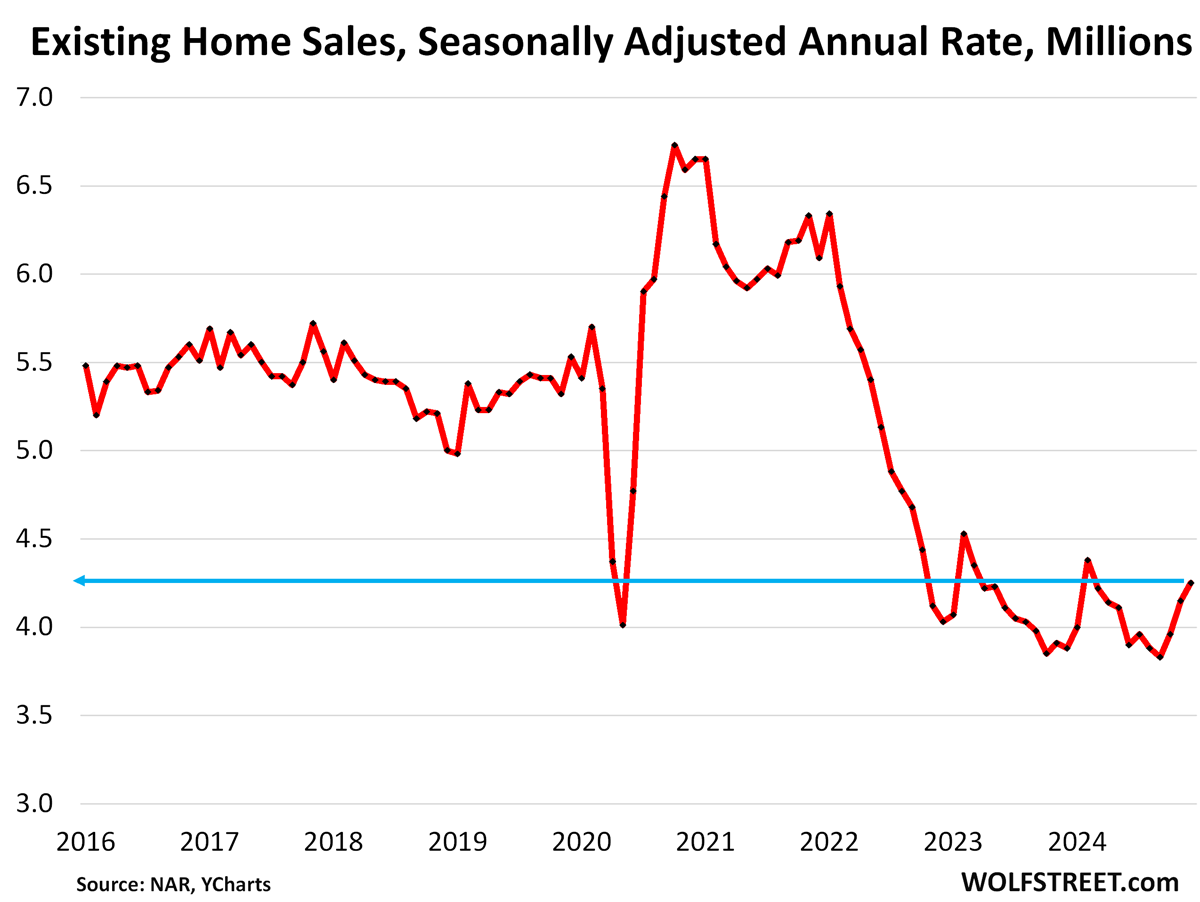

The seasonally adjusted annual rate of sales, which attempts to iron out the seasonal changes and multiplies this out to a 12-month period, rose by 2.4% in December from November to an annual rate of 4.25 million homes – down by 30% from the rate in December 2021 and by 23% from the rate in 2019, according to the National Association of Realtors today (historical data from YCharts):

For the whole year 2024, actual sales fell to 4.06 million homes, the lowest since 1995, below even the worst years during the Housing Bust, when demand destruction was caused by an economic and financial meltdown that followed years of reckless mortgage lending.

But in 2023 and 2024, demand destruction was caused by a historic spike in home prices in the prior three years, when the NAR’s national median price shot up by nearly 50% from June 2019 through June 2022 – which then collided in 2023 with mortgage rates that returned to the normal-ish levels before the money-printing era started in 2009.

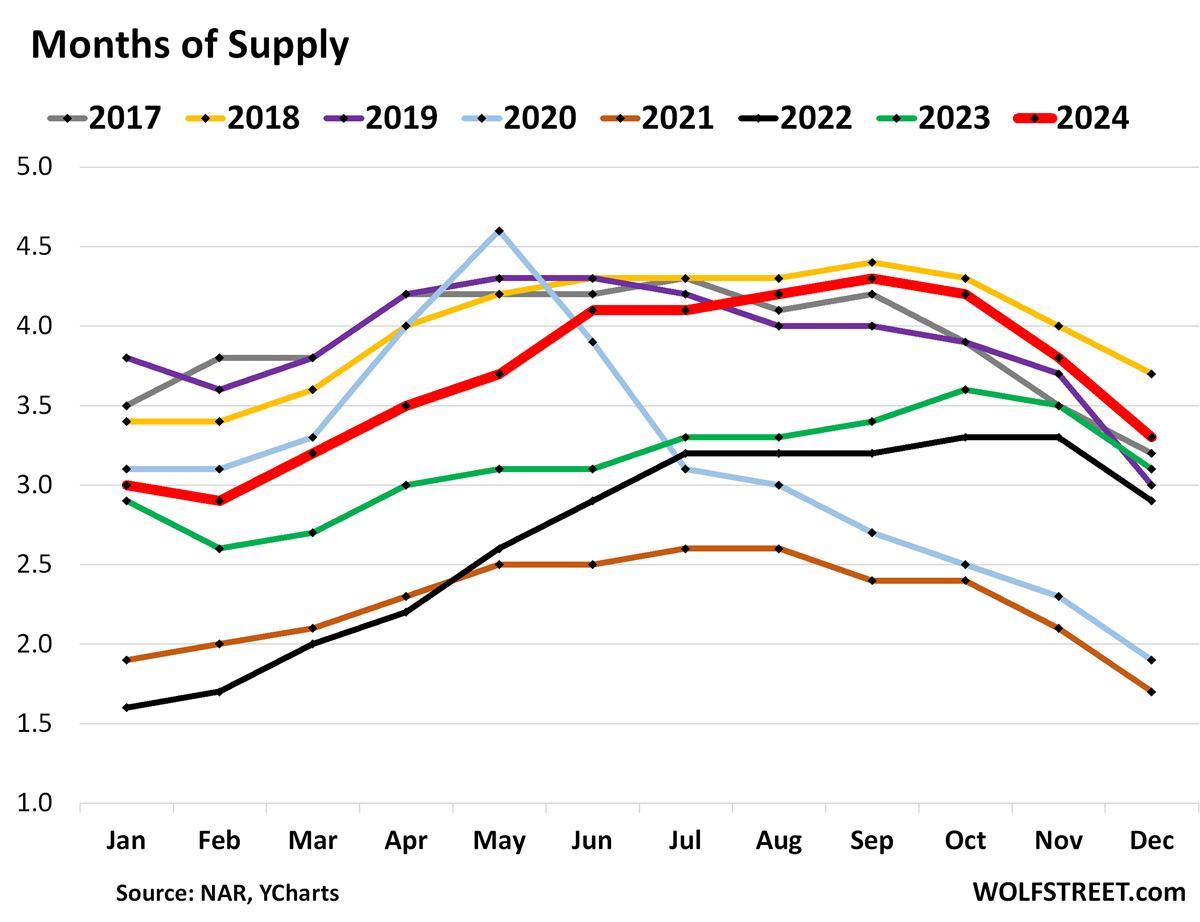

Highest supply for any December since 2018.

Supply of unsold existing homes on the market, at 3.3 months (red line in the chart below), was the highest for any December since 2018, and higher than 2017 and 2019-2023.

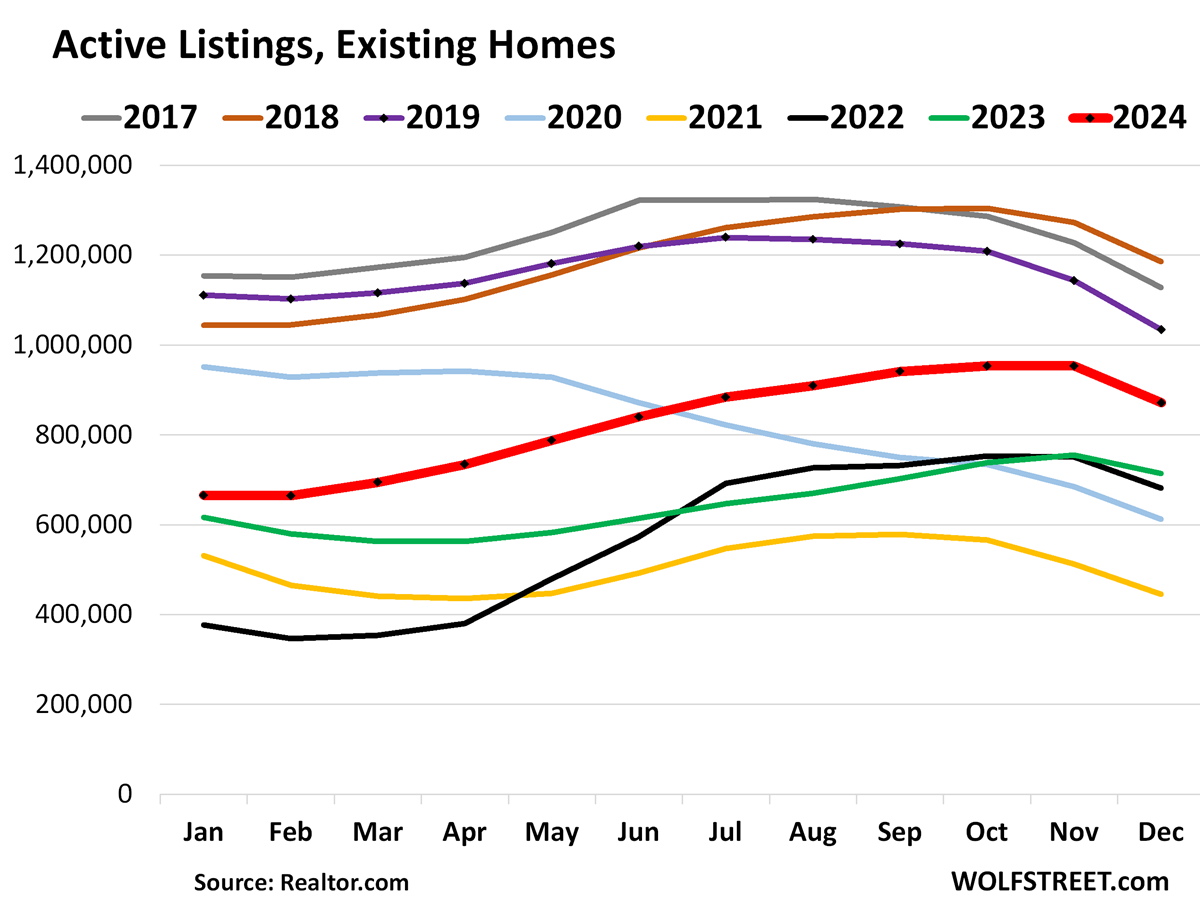

Active Listings doubled since 2021.

Active listings – total inventory for sale minus homes whose sales are pending – at 871,500 in December (bold red line), were at the highest level for any December since 2019, having nearly doubled since December 2021 amid the plunge in sales.

Unsold inventory, at 1.15 million homes, was up by 16% year-over-year. Over the holiday period in December, demand dries up, homes get pulled off the market, new listings dry up, and what is on the market, sits there longer without selling.

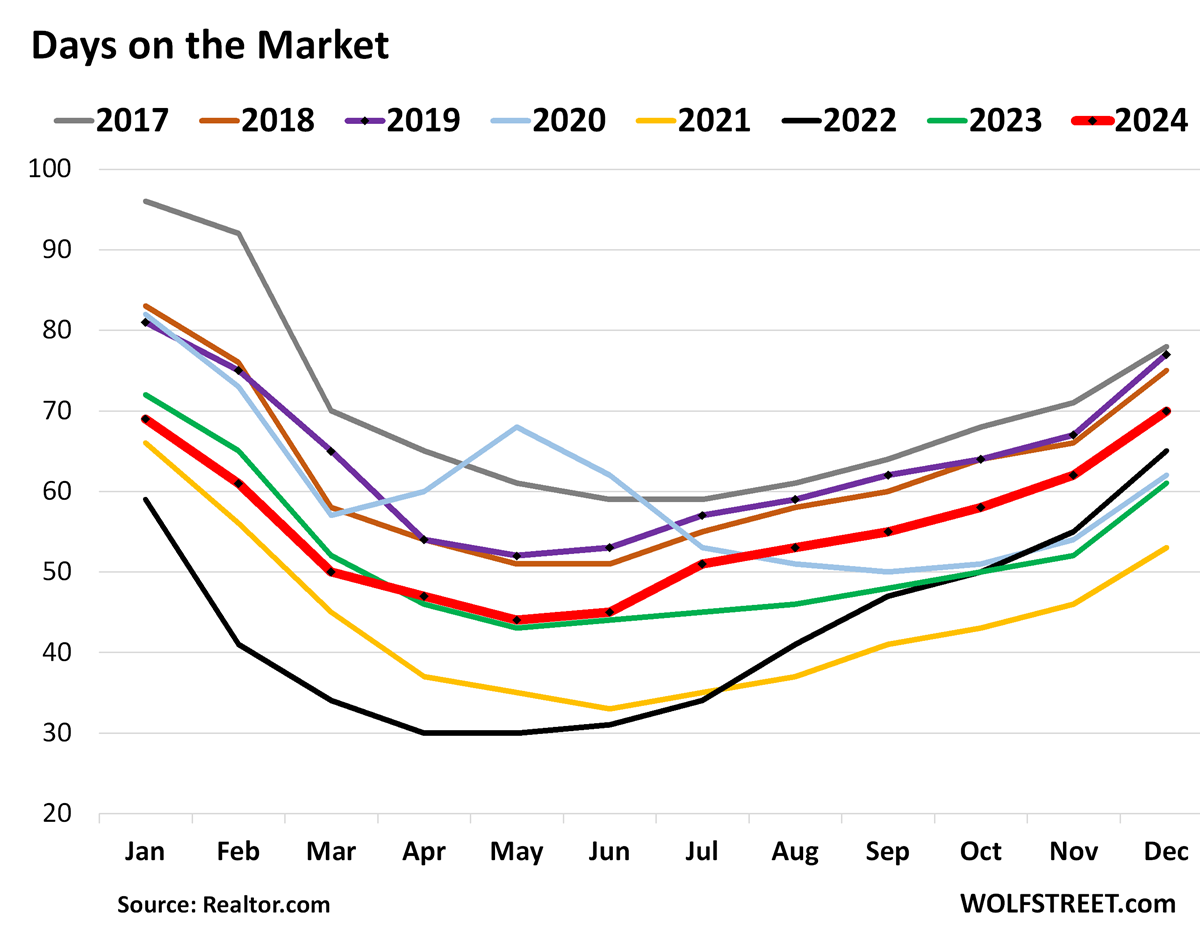

Days on the market lengthen to 70 days.

The median number of days before the home is either sold or pulled off the market because it failed to sell rose to 70 days in November, the most for any December since 2019, and up from 61 days a year ago, according to data from Realtor.com.

Days on the market track the mix of how motivated sellers are by letting their home sit on the market when it doesn’t sell right away, and how quickly homes sell that do sell.

Prices are too high.

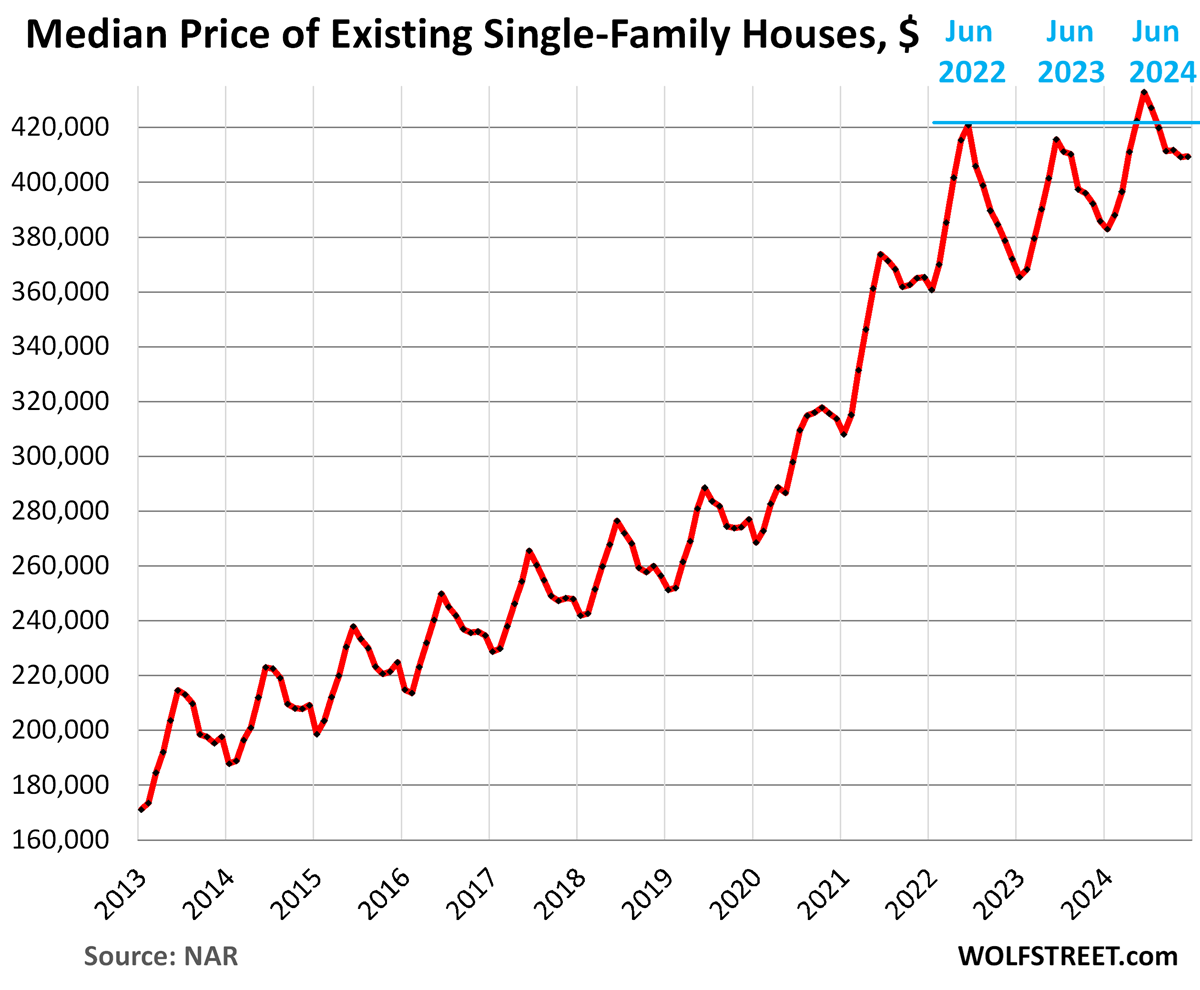

Single-family house prices. As has been the case for months, the median price of single-family houses was revised down for the prior month, which also reduced the year-over-year gain for that month. For November, the median price was revised down to $409,200 from $410,900 originally reported a month ago, which shaved the year-over-year gain for November to +4.3%, from the originally reported +4.8%. These downward revisions keep happening. I bring this up because the December year-over-year gain was an outlier of +6.1%, the highest since October 2022, but when the December median price gets revised down next month, the year-over-year gain will be back in the range of other year-over-year gains in 2004.

Based on the pre-pandemic seasonality, the median price drops sharply in January, and January-February mark the seasonal low points.

The 50% price explosion between June 2019 and June 2022, on top of the large price gains in the prior 10 years, was driven by the Fed’s interest-rate repression and money-printing schemes which have created the #1 problem in the housing market today: Prices are way too high.

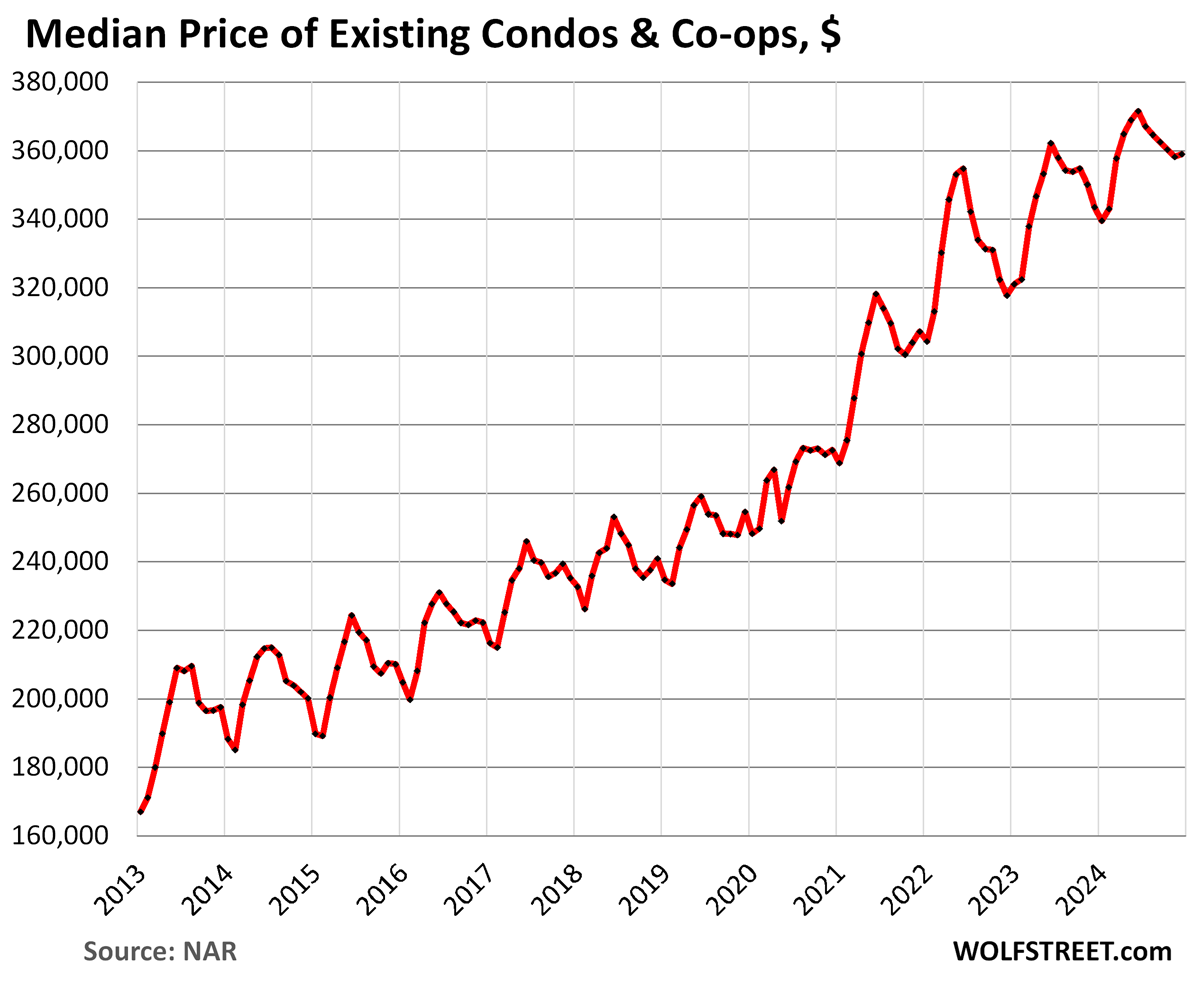

Condo and co-op prices. Here too, as has been the case for months, the median price of condos and co-ops was revised down for November to $358,200, from the originally reported $359,800. This shaved the year-over-year gain to +2.3%, from the originally reported +2.8%. And so we can expect that the December median price will also stick with tradition and get revised down as well.

As reported today, the median price in December, at $359,000, was up by 4.5% year-over-year, and we expect tradition to continue with a downward revision next month. Unlike single-family house prices, the median condo price didn’t experience year-over-year declines in mid-2023.

But home prices vary widely by metro.

In a number of the largest cities, prices of single-family houses and condos have been dropping for over two years.

Double-digit price declines of single-family houses from their respective peaks in 2022 or 2021 occurred in four of the biggest cities:

- Austin: -19%, to lowest price level since 2021

- Oakland: -17%, to lowest since 2020

- New Orleans: -17%, to lowest since 2020

- San Francisco: -15%, to lowest since 2018

Double-digit price declines of condos and co-ops from their respective peaks in 2022 or 2021 occurred in seven of the biggest cities:

- Austin: -21%, to lowest price level since 2021

- Oakland: -19%, to lowest since 2016

- San Francisco: -15%, to lowest since 2015

- Detroit: -13%, back to 2018

- New York City: -13%, back to 2017

- New Orleans: -12%, first seen in 2016

- Seattle: -10%, back to 2017.

Here are all our charts and data of the big cities with the biggest price declines from their respective peaks years ago. And here are our charts and figures of home prices in the 33 biggest metropolitan areas, from steep declines to ongoing increases, documenting the divergence in the US housing market.

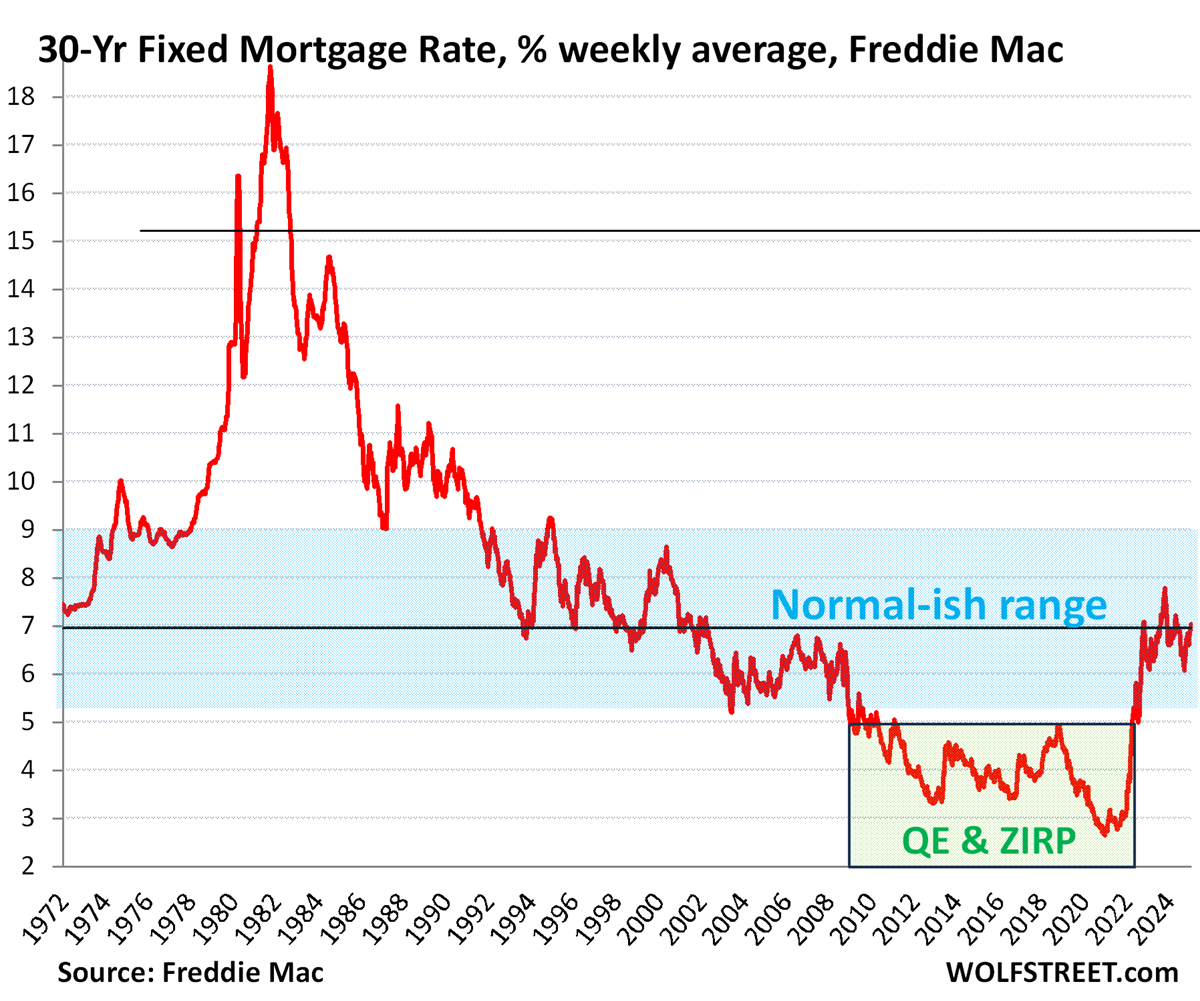

Slowly getting used to the old normal 6-7% mortgages.

The average 30-year fixed mortgage rate has been above 6% since September 2022 and above 7% on and off since October 2022. The daily measure by Mortgage News Daily is today at 7.11%. Freddie Mac’s weekly measure, released yesterday, of the average 30-year fixed mortgage rate was 6.96%.

The real estate industry has now given up waiting for mortgage rates to plunged to wherever and is encouraging sellers and buyers to get used to “a new normal of mortgage rates between 6% and 7%,” as the NAR had put it, which are the old normal rates that prevailed before the money-printing era started in 2009..

The CEO of Fannie Mae, the largest Government Sponsored Enterprise that buys and guarantees mortgages, also encouraged buyers, sellers, and everyone in the industry to get used to these 6% to 7% mortgage rates.

Before the money printing era, the average mortgage rates had been well above 5%. The Fed’s QE and zero-interest-rate policy, which started in 2008 and, with some interruptions, finally ended in 2022, had created an anomaly:

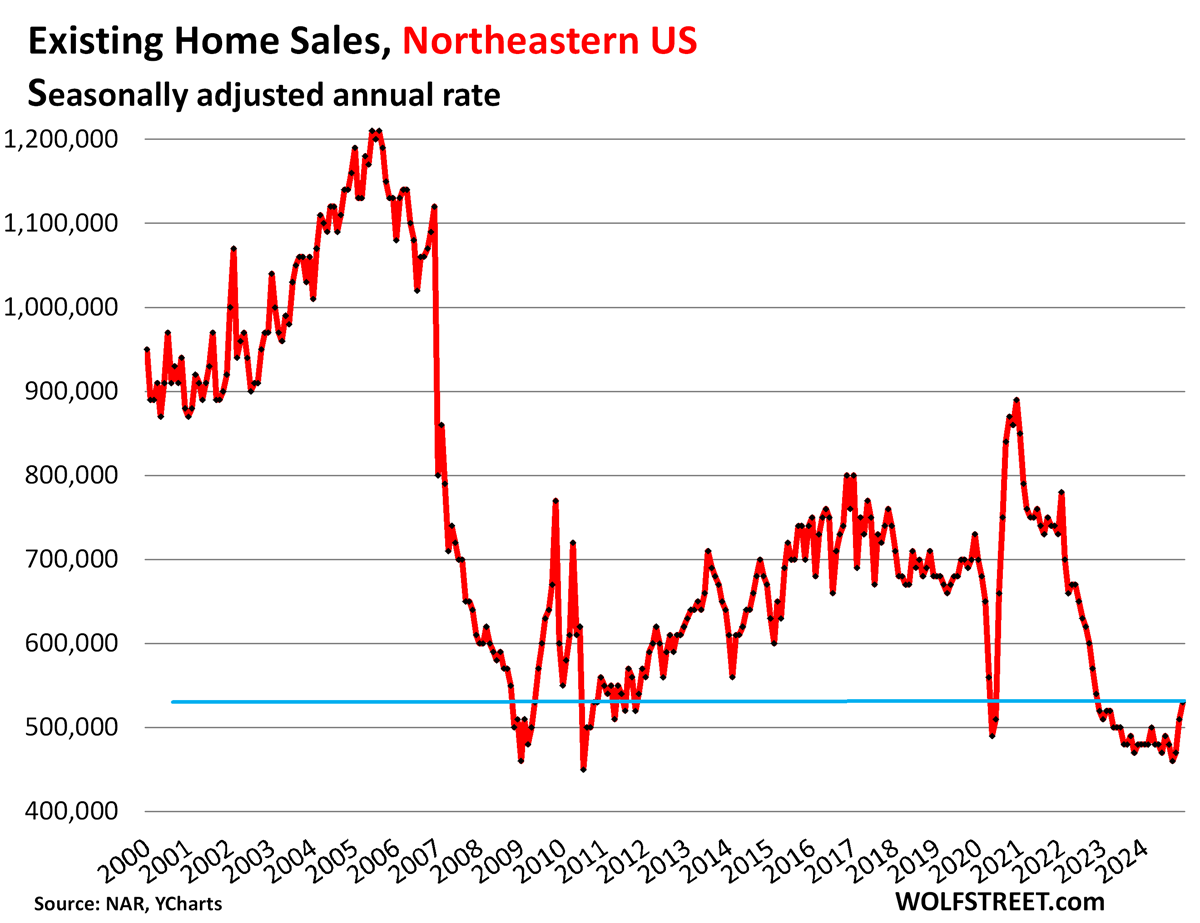

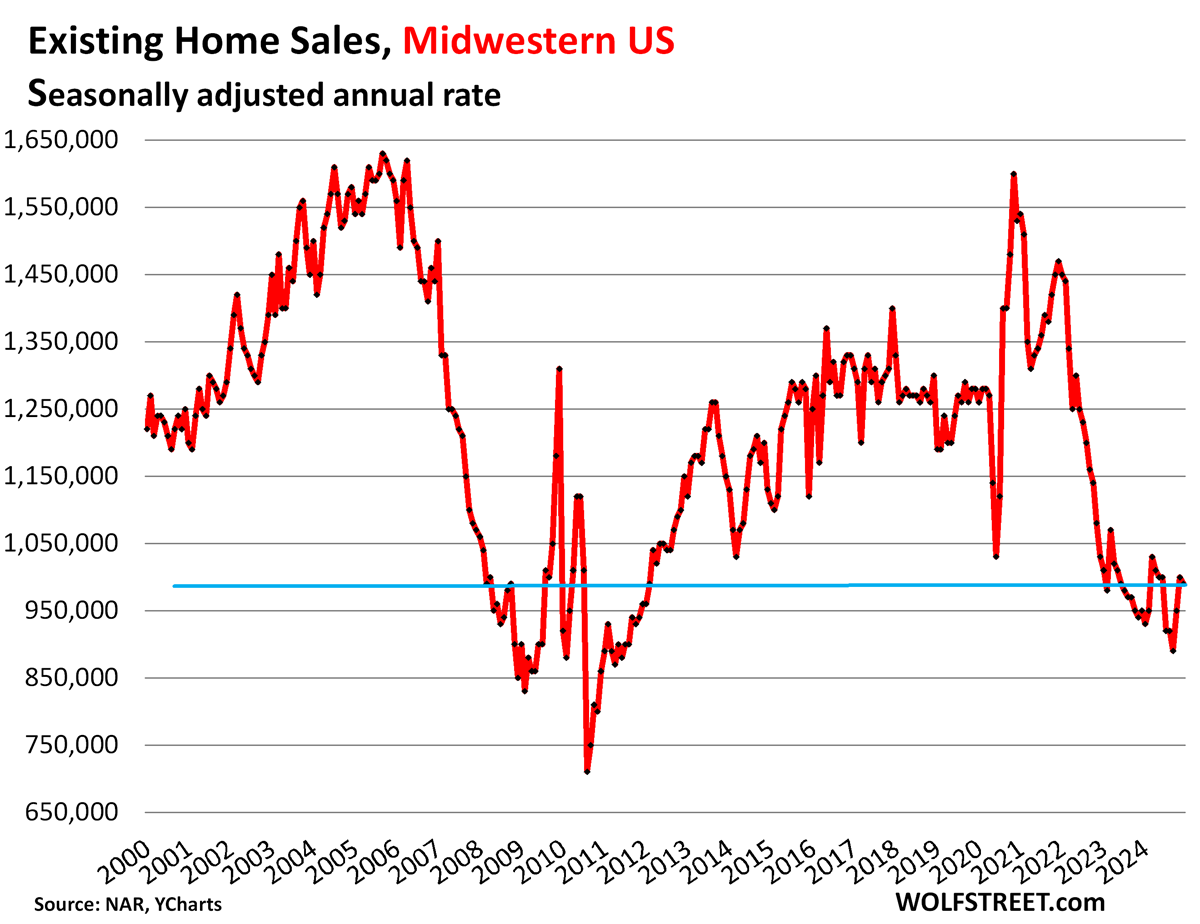

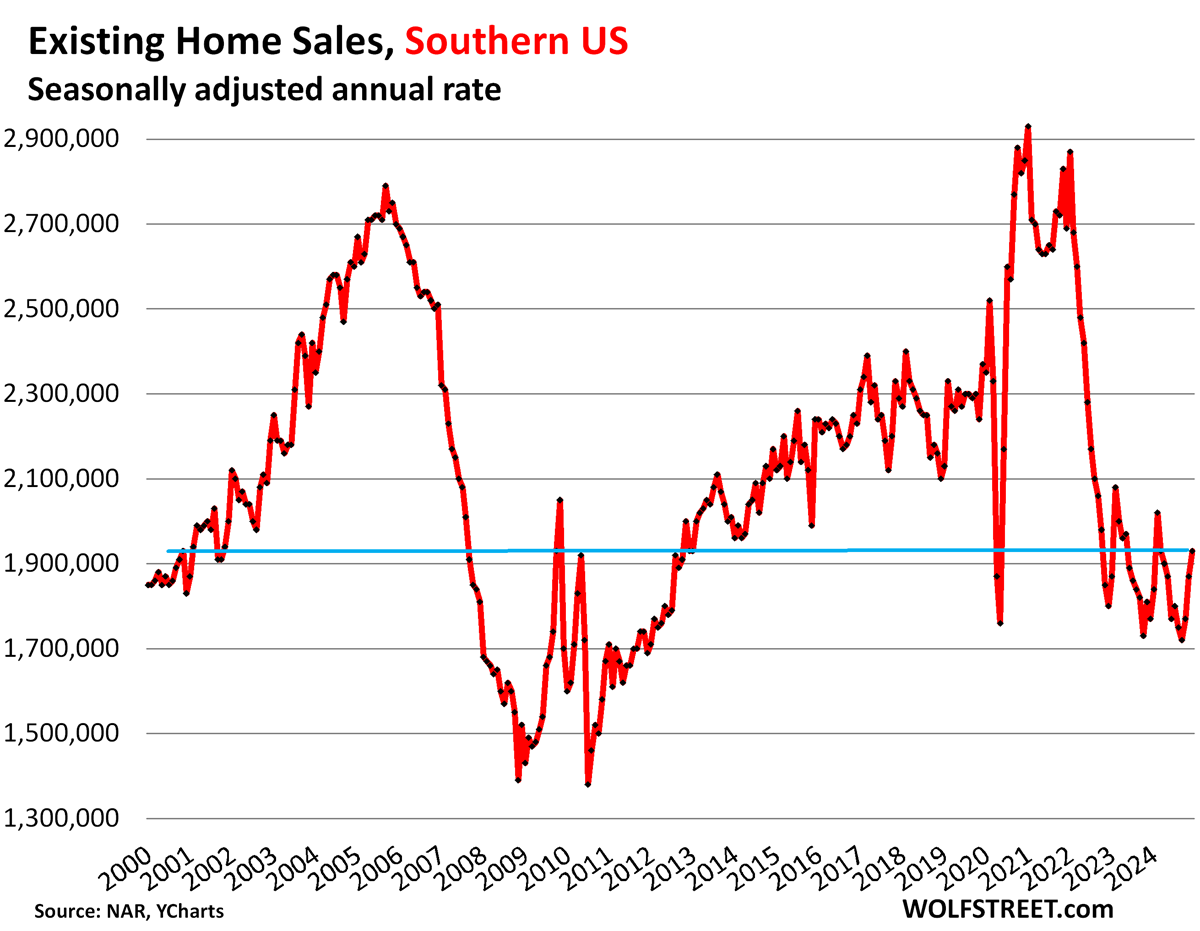

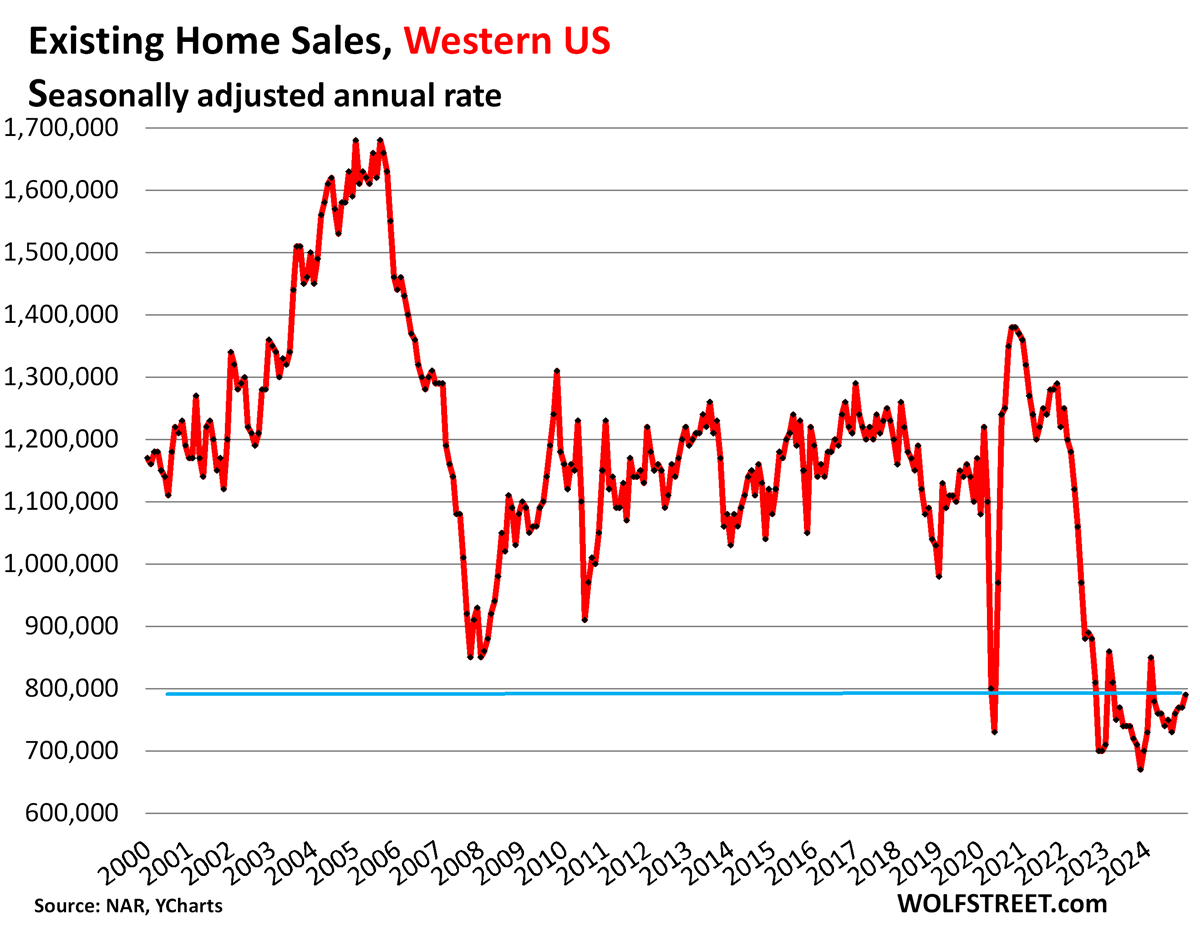

Demand destruction by region.

The charts below show the seasonally adjusted annual rate of sales, released by the NAR today, in the four Census Regions of the US. A map of the four regions is in the comments below the article.

Northeastern US: The seasonally adjusted annual rate of sales rose to 530,000 homes:

Midwestern US: The seasonally adjusted annual rate of sales dipped to 990,000 homes.

Southern US: The seasonally adjusted annual rate of sales rose to 1,930,000 homes.

Western US: The seasonally adjusted annual rate of sales rose 790,000:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post Sales of Existing Homes Finally Begin to Thaw a Little, amid Highest Supply for December since 2018 appeared first on Energy News Beat.

“}]]