[[{“value”:”

The office-debt meltdown keeps getting worse. The motto in 2024 was “Survive till 2025” via extend-and-pretend. But now what?

By Wolf Richter for WOLF STREET.

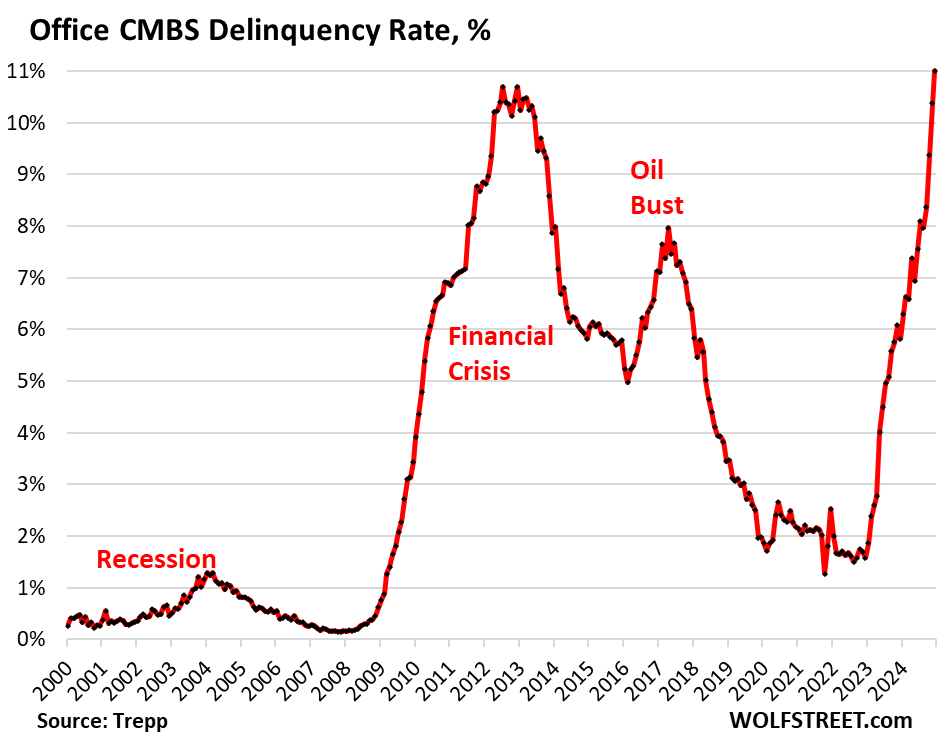

The delinquency rate of office mortgages that have been securitized into commercial mortgage-backed securities (CMBS) spiked to 11.0% in December, a new all-time high, surpassing even the debt-meltdown during the Financial Crisis, when office CMBS delinquency rates peaked at 10.7%, according to data by Trepp today, which tracks and analyzes CMBS.

Over the past 24 months, the delinquency rate for office CMBS has exploded by 9.4 percentage points, from 1.6% to 11.0%, from everything-is-just-fine to disaster.

The office sector of commercial real estate is in a depression, and office debt just keeps getting worse: an additional $2 billion in CMBS office debt became newly delinquent in December.

Of the major sectors in CRE, office debt is in the worst shape, with its CMBS delinquency rate of 11.0%, compared to lodging (6.1%), permanently troubled retail (7.4%), and multifamily (4.6%). But CRE debt on industrial properties, such as warehouses and fulfillment centers, thanks to the continued boom of ecommerce and the brick-and-mortar infrastructure it requires, remains in pristine condition with a delinquency rate of just 0.3%.

The “flight to quality” split the office market in two. High vacancy rates in the latest and greatest buildings allow companies to move from an older office tower into new fancy digs, while downsizing office space at the same time. As they leave older office towers, new tenants to replace them are hard to find, and the vacancy rates of those older office towers skyrockets, thereby speeding up their demise. It’s those older office towers that are on the problem list, not the latest and greatest towers.

Mortgages count as delinquent when the landlord fails to make the interest payment after the 30-day grace period. A mortgage doesn’t count as delinquent if the landlord continues to make the interest payment but fails to pay off the mortgage when it matures, which constitutes a repayment default. If repayment defaults by a borrower who is current on interest were included, the delinquency rate would be higher still.

Loans are pulled off the delinquency list when the interest gets paid, or when the loan is resolved through a foreclosure sale of the property, or a sale of the loan, generally involving big losses for the CMBS holders, or if a deal gets worked out between landlord and the special servicer that represents the CMBS holders, such as the mortgage being restructured or modified and extended – the infamous extend-and-pretend.

Extend and pretend has been a feature in 2024, and as a result, the problems are getting dragged into 2025. Extend and pretend can get lenders through a temporary crisis, but not through this kind of structural reckoning.

Extend and pretend came with the motto, “survive till 2025,” because, you know, in 2025, the structural problems of office CRE would somehow go away as the Fed would cut interest rates back to zero, or whatever.

The structural problem is that no one needs all this office space, amid huge vacancy rates in office buildings across the US. Landlords default on their interest payments because they don’t collect enough in rents in their semi-vacant buildings to pay interest and other costs. And they can’t refinance maturing loans when the building doesn’t generate enough in rents to cover interest and other costs. And they cannot sell the office tower and pay off the loan because prices of older office towers have collapsed by 50%, 60%, 70%, or more, and in some cases, office towers sold for land value.

The glut is a result of years of overbuilding amid hype of an “office shortage” that led companies to grab office space as soon as it came on the market to grow into it later. But during the pandemic, they realized they don’t need this unused office space, and they put it on the market for sublease, adding to the office glut.

The Fed has cut interest rates by 100 basis points, but at its December meeting projected only 50 basis points in cuts for 2025, and during the press conference, Powell threw some doubts on those, lamenting that the Fed still had “some work to do” amid re-accelerating inflation in an economy that is growing well above its 15-year average.

A lot of CRE loans are floating-rate loans whose interest rate is pegged to short-term rates, such as an average of SOFR. Lower short-term rates bring some relief, but won’t solve the structural glut of office buildings, and owners of nearly empty older office towers still won’t be able to make the interest payments even at lower interest rates.

A good thing for US banks is that a big part of office mortgages has been broadly spread across investors around the world, via CMBS and CLOs, or directly. They’re held by bond funds, pension funds, insurers, private and publicly-traded office REITs, mortgage REITS, PE firms, private-credit firms, and of course foreign banks. Those mortgages not held by US banks pose no threat to the US banking system.

But US banks also hold a pile of office loans, and some have already disclosed big write-downs of their office loans, so some of that stuff is getting cleaned up, but lots of troubled mortgages were extended in 2024, and now there’s 2025, and regulators are getting impatient with this extend-and-pretend.

The office-debt write-downs dent or demolish earnings for a quarter or two, and the stock drops, and maybe some smaller banks will choke on their office debt and collapse, but that hasn’t happened yet.

Office debt alone isn’t big enough – at less than $1 trillion, it accounts for only about 16% of total CRE debt – and is held too broadly by investors, such as these hapless CMBS holders, to do serious damage to the US banking system.

Office-to-residential conversions are only feasible for some office towers. See my discussion and figures at the top of the comments below.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post Office CMBS Delinquency Rate Spikes to a Record 11%, Blowing by the Financial Crisis Peak appeared first on Energy News Beat.

“}]]