[[{“value”:”

ENB Pub Note: This is great news for the US economy and environment. As Natural Gas is critical to export, and electrical generation, it is often just flared as the pipeline capacity has been limited. Capturing stranded gas for Bitcoin mining or localized electricity generation has been beneficial, but pipelines are critical for long-term growth and positive environmental impact.

Summary

- Continued growth in Permian natural gas production will require incremental takeaway, with a few projects announced in recent months.

- Growing natural gas demand is also supporting pipeline opportunities for midstream, including new pipeline capacity to supply LNG export facilities.

- Midstream companies focused on natural gas pipelines and gathering and processing businesses can stand to benefit from increased production and new demand for natural gas.

Texas is the center of the US energy industry, home to significant oil and natural gas production and growing energy export capacity along the Gulf Coast. Specific to natural gas, more pipeline infrastructure is needed to connect Permian production with demand, while additional pipeline capacity is needed to supply liquefied natural gas (LNG) export facilities. This note looks at some of the pipeline projects in Texas under development, the underlying themes driving investment, and the companies set to benefit from the increased capacity.

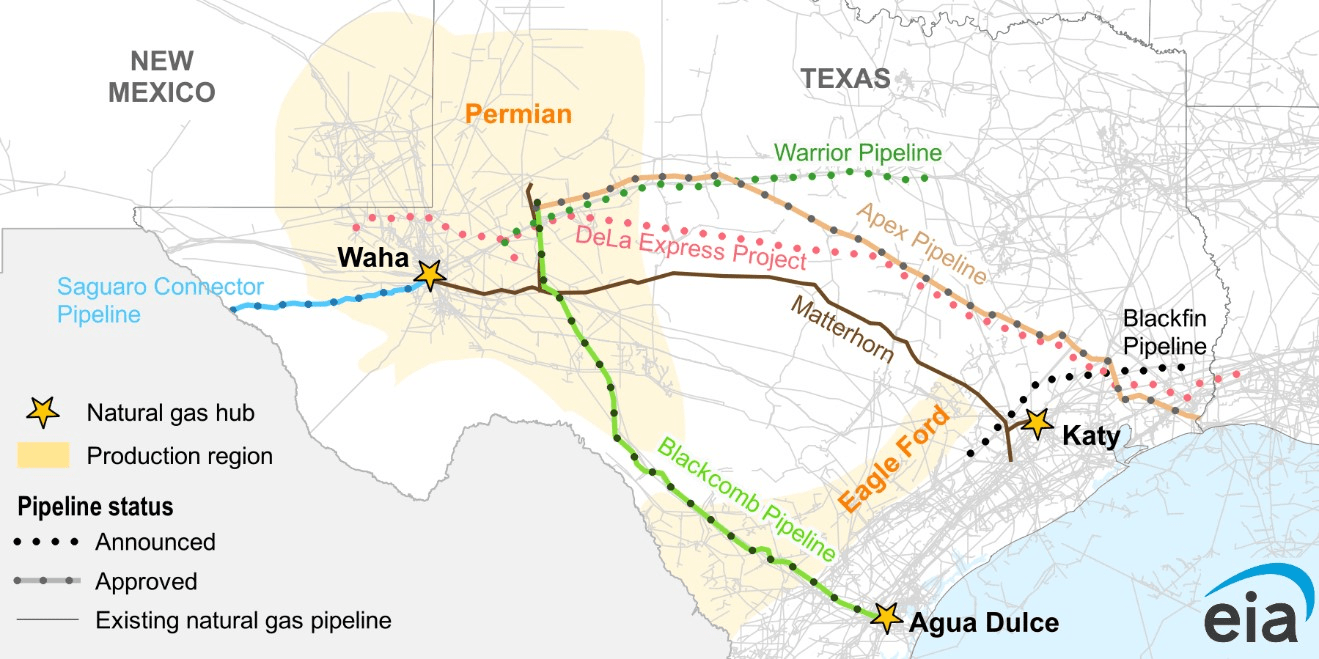

Supply Push for Permian Natural Gas

A robust, multi-year outlook for US natural gas demand growth should support rising US gas production in the coming years (read more), but in the Permian, natural gas volumes have been increasing as a function of oil production. Much of the natural gas produced in the Permian is “associated gas” or gas produced as a byproduct from oil wells. As a result, natural gas production is driven more by oil prices. Additionally, the Permian has become gassier over time, with higher amounts of gas being produced per barrel of oil.

The Permian Basin is driving production growth in Texas, which produces more natural gas than any other state in the US. Permian natural gas production has outpaced pipeline capacity, causing deep discounts in regional natural gas prices, including negative prices at the Waha hub (read more). Production in the Permian basin is forecasted to grow by another 1.3 billion cubic feet per day (Bcf/d) for 2025 based on annual averages.

Pipeline Projects Advance for Permian Takeaway

Natural gas egress out of the Permian has been a bottleneck as production growth has outpaced pipeline capacity additions. With natural gas production continuing to grow, even more pipeline capacity will be needed out of the Permian.

For context, raw natural gas is gathered from wells and brought to processing plants. Once processed, natural gas can be transported through larger pipelines connecting natural gas hubs like Waha in West Texas or Katy near Houston, as shown in the map below. The Matterhorn Express Pipeline, which began service on October 1, added 2.5 Bcf/d of natural gas pipeline capacity out of the Permian to the Houston area.

In 2H24, two newbuild pipelines and a pipeline expansion project were sanctioned that will bring additional capacity out of the Permian beginning in 2026. The Hugh Brinson (formerly Warrior) and Blackcomb pipelines are the two greenfield projects that reached a final investment decision (FID) in 2024. At FID, a company formally commits to move forward with a project, having secured sufficient customer interest (read more).

Phase 1 of Hugh Brinson will add 1.5 Bcf/d of capacity, and Phase 2 could increase the capacity to 2.2 Bcf/d, according to operator Energy Transfer (ET). The pipeline will run from Waha to ET’s pipeline and storage assets south of Dallas, where it will connect to existing pipelines with access to markets across Texas.

Meanwhile, Blackcomb, owned by affiliates of WhiteWater Midstream, MPLX (MPLX), Enbridge (ENB, ENB:CA), and Targa Resources (TRGP), will connect Permian gas to the Agua Dulce hub in South Texas. Blackcomb will add 2.5 Bcf/d of pipeline capacity out of the Permian. Shippers include Devon Energy (DVN), Diamondback Energy (FANG), Marathon Petroleum (MPC), and TRGP.

The third project to reach FID in 2H24 was the 0.57 Bcf/d expansion of Gulf Coast Express (GCX) that goes from Waha to the Agua Dulce hub. GCX is now jointly owned by Kinder Morgan (KMI), which operates the pipeline, and ArcLight Capital Partners, which acquired a 16% and 25% interest in 2024.

(Source: Energy Information Administration)

Demand Pull Pipeline Opportunities Headlined by LNG

While the pipelines discussed above are driven by production growth (supply push), incremental demand can also require new pipeline capacity. These pipelines are described as demand pull. There are multiple drivers for US natural gas demand growth in the coming years, but the biggest ones tend to be LNG exports and power generation, including for data centers (read more).

LNG export capacity is expanding along the Texas Gulf Coast from Port Arthur to Brownsville (read more). Supplying these facilities requires more gas pipeline capacity. These tend to be shorter pipelines transporting gas from trading hubs directly to the LNG facility.

For example, to facilitate Cheniere Energy’s (LNG) Corpus Christi Stage III expansion, more feed gas is needed. In July, the ADCC pipeline, owned by Cheniere and Whistler Pipeline, began service and can transport up to 1.7 Bcf/d of gas from Agua Dulce. Further south, the Rio Bravo Pipeline, being built by ENB and expected to come on-line in 2026, will supply up to 4.5 Bcf/d of natural gas to Next Decade’s Rio Grande LNG facility in South Texas.

How Do Investors Gain Exposure to Natural Gas Pipeline Growth?

Incremental production growth and new sources of demand are creating growth opportunities for pipeline companies. Given the constructive outlook, investors could seek greater exposure to North American energy infrastructure companies with natural gas assets.

The Alerian Midstream Energy Select Index (AMEI) includes midstream C-Corps and MLPs that own and operate natural gas infrastructure, including pipelines. ET, ENB, KMI, MPLX, LNG, and TRGP are all constituents of AMEI. As of December 17, 75.5% of AMEI by weighting primarily generates cash flow from natural gas infrastructure. This percentage include companies focused on long-haul natural gas pipelines, as well as names focused on gas gathering and processing and liquefaction.

Bottom Line

In Texas, Permian natural gas production growth and additional LNG export capacity are creating attractive pipeline opportunities for midstream companies.

AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX).

Disclosure: © VettaFi LLC 2025. All rights reserved. This material has been prepared and/or issued by VettaFi LLC (“VettaFi”) and/or one of its consultants or affiliates. It is provided as general information only and should not be taken as investment advice. Employees of VettaFi are prohibited from owning individual MLPs. For more information on VettaFi, visit VettaFi.

The post Natural Gas Pipeline Capacity Ramping Up In Texas appeared first on Energy News Beat.

“}]]