[[{“value”:”

ENB Pub Note: This is essential data from the EIA as it will consider how much trade tariffs can be offset by energy exports. In my Substack article “U.S. LNG Exports are Trump’s Trade Right Sizing Ace in his pocket”, I covered the volume that the LNG exports could cover in trade imbalances. US LNG exports were an estimated 24 billion dollars.

Note: Earlier scenario assumes start-up dates two-to-five months earlier than announced by project developers; Later scenario assumes start-up dates six months later than announced by project developers.

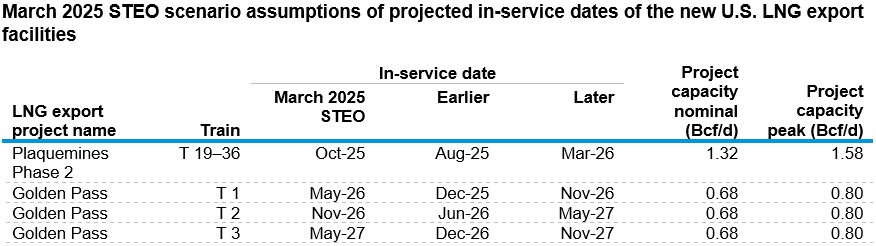

U.S. exports of liquefied natural gas (LNG) represent the largest source of natural gas demand growth in our March 2025 Short-Term Energy Outlook (STEO), with LNG gross exports expected to increase by 19% to 14.2 billion cubic feet per day (Bcf/d) in 2025 and by 15% to 16.4 Bcf/d in 2026. The start-up timing of two new LNG export facilities—Plaquemines LNG Phase 2 (consisting of 18 midscale trains) and Golden Pass LNG—could significantly affect our forecast because these facilities represent 19% of incremental U.S. LNG export capacity in 2025–26.

To illustrate the possible range of outcomes, we varied the assumed start-up dates of these new facilities compared with the baseline in our March 2025 STEO. This enabled us to quantify the changes in natural gas feedgas demand that would result from earlier or later start-up dates and discuss the implications for domestic supply-demand balances, prices, and storage. This analysis is limited only to the effects on natural gas; we did not examine the repercussions of each scenario on other areas of the energy sector.

Which projects are driving the increase in LNG exports?

LNG exports from the United States have increased every year since 2016, rising from 0.5 Bcf/d in 2016 to 11.9 Bcf/d in 2024, making the United States the world’s largest LNG exporter in 2023 and 2024. Increasing international demand for natural gas and the buildout of U.S. LNG export facilities have enabled this growth. We expect U.S. LNG exports to continue growing, driven by the start-up of three new facilities: Plaquemines LNG (Phases 1 and 2), Corpus Christi LNG Stage 3, and Golden Pass LNG. These facilities have a combined nominal export capacity of 5.3 Bcf/d (up to 6.3 Bcf/d peak capacity) and will expand the existing U.S. LNG export capacity by almost 50% once these projects become fully operational. Plaquemines LNG Phase 1 started LNG exports in December 2024, and we assume that this facility will fully ramp up by April 2025. Corpus Christi Stage 3 produced its first LNG cargo in February 2025, and we assume that the project will place all seven midscale trains in service by the end of 2026.

Note: Bcf/d=billion cubic feet per day; LNG=liquefied natural gas

What scenarios did we develop and analyze?

The start-up timing of exports, or in-service date (ISD), for Golden Pass and Plaquemines LNG Phase 2 is uncertain and could affect our STEO forecast of natural gas supply and demand balances, storage, and prices. Differences between our estimate of a project’s ISD and the actual ISD can arise due to accelerated or delayed construction times, for example.

We developed two scenarios around our March 2025 STEO—the Earlier scenario, which assumed start-up dates two-to-five months earlier than announced by project developers, and the Later scenario, which assumed start-up dates six months later than announced by project developers.

Note: Consistent with Venture Global’s initial regulatory filings, we use Plaquemines Phase 2 to refer to the project’s Blocks 10–18 (corresponding to Trains 19–36); each block contains two single mixed refrigerant process trains, a refrigerant storage site, and piping that connects the refrigerant storage site and the process trains. Golden Pass T2 and T3 fall into or out of the STEO forecast depending on the in-service date. The March Short-Term Energy Outlook (STEO) forecast period ends in December 2026; any in-service date later than that is not included in our STEO forecast. The Earlier scenario assumes start-up dates two-to-five months earlier than announced by project developers; the Later scenario assumes start-up dates six months later than announced by project developers. Bcf/d=billion cubic feet per day

The assumed ISDs of the new U.S. LNG export facilities in our March 2025 STEO are based on public announcements by the terminal developers and filings with the Federal Energy Regulatory Commission (FERC). We assume each facility undergoes an initial ramp-up period during which it operates below its nominal capacity while the developers gradually prepare various systems to enter full production mode. When the ramp-up period ends but before commercial service with the start of long-term contracts begins, we assume LNG exports from the new facilities will be dispatched based on global demand.

In each of the scenarios, we applied the same assumptions of ramp-up periods for the new LNG export facilities, during which liquefaction trains are gradually brought up to full production capacity over a period of several months.

Note: Liquefied natural gas (LNG) export capacity of the new projects is the nominal capacity. The Earlier scenario assumes start-up dates two-to-five months earlier than announced by project developers; the Later scenario assumes start-up dates six months later than announced by project developers.

How could various start-up dates affect U.S. LNG export volumes?

Compared with the March 2025 STEO, U.S. LNG exports are lower in the Later scenario and higher in the Earlier scenario; the largest volume difference in both scenarios occurs in 2026. The Earlier scenario results in 0.2 Bcf/d more LNG exports in 2025 and 0.5 Bcf/d more LNG exports in 2026 compared with the March STEO. The Later scenario results in 0.2 Bcf/d fewer LNG exports in 2025 and 0.8 Bcf/d fewer LNG exports in 2026.

Note: The Earlier scenario assumes start-up dates two-to-five months earlier than announced by project developers; the Later scenario assumes start-up dates six months later than announced by project developers. LNG=liquefied natural gas

How could differences in LNG exports affect U.S. natural gas prices and inventories?

In the March 2025 STEO, annual demand exceeds supply in both 2025 and 2026, leading to lower inventories and increasing Henry Hub prices in both years. We forecast the Henry Hub natural gas spot price will almost double from an average of about $2.20 per million British thermal units (MMBtu) in 2024 to an average of nearly $4.20/MMBtu in 2025 and increase an additional 7% to average just under $4.50/MMBtu in 2026.

Varying levels of LNG exports translate directly to changes in demand for domestic natural gas to supply feedgas to the LNG facilities, affecting natural gas inventories, supply, and prices. For example, in the Later scenario where LNG exports are lower compared with the March 2025 STEO, we would expect to see reduced feedgas demand result in higher volumes of natural gas in underground storage, all else being equal, that would also likely result in lower natural gas prices. Conversely, higher LNG exports in the Earlier scenario would result in lower volumes in underground storage and likely higher natural gas prices, all else being equal.

Lower natural gas prices tend to lead to more consumption of natural gas in the electric power sector because of the flexibility in that sector to switch between fuel sources. This increased consumption in the electric power sector would lead to more overall natural gas demand, offsetting the lower demand for LNG exports that results from our Later scenario. Higher natural gas prices, which could result from our Earlier scenario, tend to decrease demand for natural gas in the electric power sector, potentially offsetting some of the increased demand for LNG exports in that scenario.

On the supply side, changes in natural gas prices tend to affect domestic natural gas production with a delay of about six months, with lower prices typically resulting in lower production and higher prices typically resulting in higher production. Natural gas price changes mainly affect regions that produce mostly natural gas with limited co-production of crude oil and other liquids, such as in the Haynesville and Appalachia regions. Natural gas production in areas such as the Permian region, where natural gas production is primarily associated natural gas, tends to not be affected as much by changes in the natural gas price alone. As new LNG facilities on the Gulf Coast begin operating, we expect natural gas production—particularly in the Haynesville region because of its proximity to these facilities—would increase to meet the increased demand.

EIA Principal contributors: Victoria Zaretskaya, Corrina Ricker

The post How will the start-up timing of the new U.S. LNG export facilities affect our forecast? appeared first on Energy News Beat.

“}]]