Authored by Yves Smith via NakedCapitalism.com,

The incompetence of our financial regulators, most of all the Fed, is breathtaking. The great unwashed public and even wrongly-positioned members of the capitalist classes are suffering the consequences of Fed and other central banks being too fast out of the gate in unwinding years of asset-price goosing policies, namely QE and super low interest rates. The dislocations are proving to be worse than investors anticipated, apparently due to some banks having long-standing risk management and other weaknesses further stressed, and other banks that should have been able to navigate interest rate increases revealing themselves to be managed by monkeys.

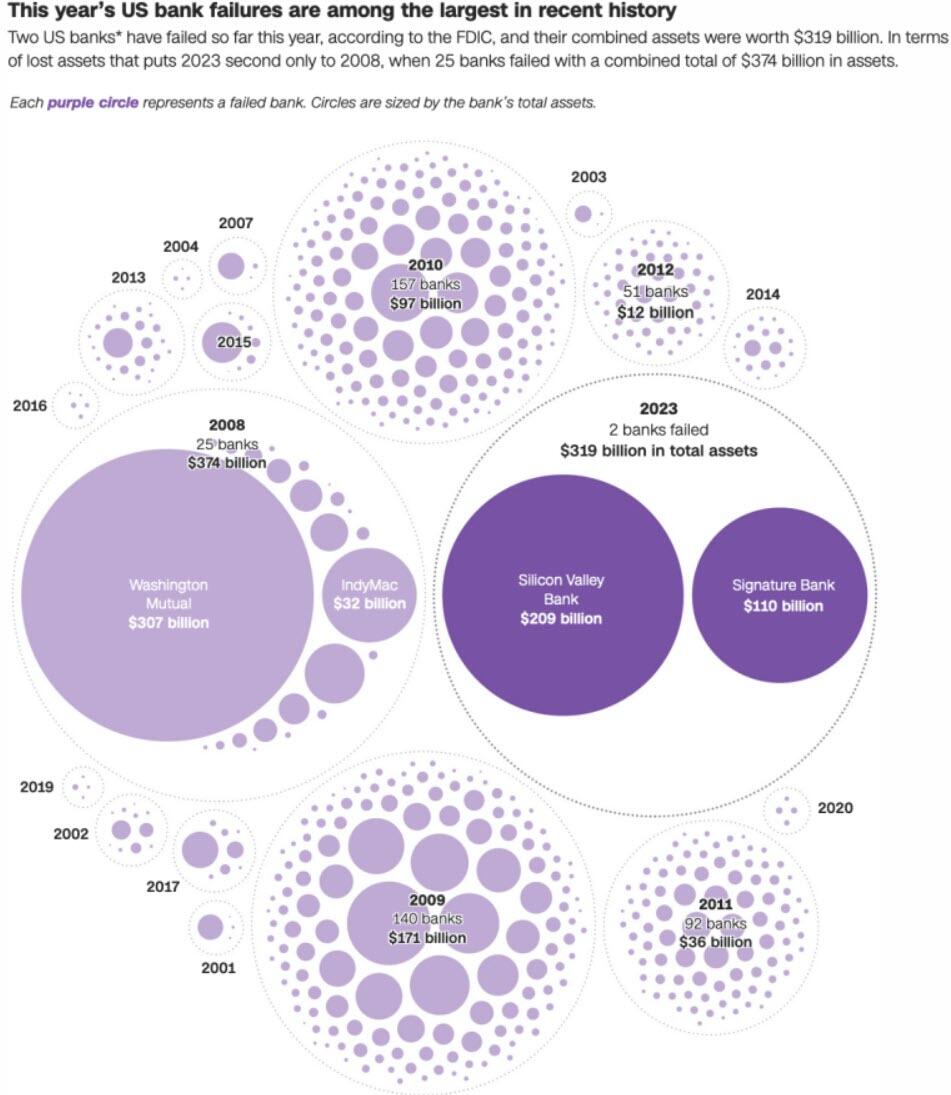

What is happening now is the worst sort of policy meets supervisory failure, of not anticipating that the rapid rate increases would break some banks. Here we are, in less than two weeks, at close to the same level of bank failures as in the 2007-2008 financial crisis. From CNN:

{kind=link}

And even mainstream media outlets are fingering the Fed:

As we’ll explain in due course, the regulators’ habitual “bailout now, think about what if anything to do about taxpayer/systemic protection later” is the worst imaginable response to this mess. For instance, US authorities have put in place what is very close to a full backstop of uninsured deposits (with ironically a first failer, First Republic, with its deviant muni-bond-heavy balance sheet falling between the cracks). But they are not willing to say that. So many uninsured depositors remained in freakout mode, not understanding how the facilities work. Yet the close-to-complete backstop of uninsured deposits amounted to another massive extension of the bank safety net.

The ultimate reason the Fed did something so dopey as to put through aggressive rate hikes despite obvious bank and financial system exposure was central bank mission creep, of taking up the mantle of economy-minder-in-chief. That was in tune with the widespread acceptance of neoliberal views of minimizing not just oversight and regulation but also overt microeconomic policy. Can’t be choosing winners and losers, national interest be damned.

That orientation allowed the executive branch and Congress to engage in pork-oriented economic policy, resulting in industrial policy by default that bloated preferred sectors like the military industrial complex, the medical industry, higher education, real estate, and finance. But it is Congress and the Administration that have the much greater ability to devise and implement more targeted programs, and make a point of favoring ones that are countercyclical.

Instead we have the Fed using the blunt instrument of interest rates to try to crush labor, when unlike the 1970s, labor bargaining power is weak and this inflation is largely the result of supply issues. As we predicted, the only way for te Fed get inflation down via interest rate increase would be to kill the economy stone cold dead. It appears to be reaching that end faster than anticipated by killing banks.

Mind you, reversing super low interest rate policies would inevitably lower asset prices, particularly those of highly-responsive financial assets. But there are better and worse ways to administer painful remedies, and the Fed has been particularly inept. The central bank did do one thing right, which was to signal its rate increases way in advance. But it bizarrely ignored how the crypto collapse might affect depositor/investor perceptions of risk. And per the New York Times, it saw serious problems at Silicon Valley Bank, yet the official strictures didn’t rise to the level of wet noodle lashings:

In 2021, a Fed review of the growing bank found serious weaknesses in how it was handling key risks. Supervisors at the Federal Reserve Bank of San Francisco, which oversaw Silicon Valley Bank, issued six citations. Those warnings, known as “matters requiring attention” and “matters requiring immediate attention,” flagged that the firm was doing a bad job of ensuring that it would have enough easy-to-tap cash on hand in the event of trouble.

But the bank did not fix its vulnerabilities. By July 2022, Silicon Valley Bank was in a full supervisory review — getting a more careful look — and was ultimately rated deficient for governance and controls. It was placed under a set of restrictions that prevented it from growing through acquisitions. Last autumn, staff members from the San Francisco Fed met with senior leaders at the firm to talk about their ability to gain access to enough cash in a crisis and possible exposure to losses as interest rates rose.

It became clear to the Fed that the firm was using bad models to determine how its business would fare as the central bank raised rates: Its leaders were assuming that higher interest revenue would substantially help their financial situation as rates went up, but that was out of step with reality.

By early 2023, Silicon Valley Bank was in what the Fed calls a “horizontal review,” an assessment meant to gauge the strength of risk management. That checkup identified additional deficiencies — but at that point, the bank’s days were numbered.

This shows that the Fed actually knew what a hot mess Silicon Valley Bank was, using risk models that assured it would be positioned 180 degrees wrong in the event of the absolutely gonna happen Fed interest rate increases.

And what did the regulator do? Scold and restrict acquisitions. Help me. That plus restricting dividends was the sanction the Fed has sometimes applied to wayward big banks. But the Fed made public these big banks were in the doghouse, using shareholders to punish bank executives (remember all big US concerns have stock-price-linked executive pay). And these big banks are presumed to be in the business of consolidation, so barring acquisitions is a bit of a ding. By contrast, Silicon Valley Bank had just acquired Boston Private in July 2021, so it’s not as if it would be likely to be on the acquisition trail any time soon.

The New York Times makes much of weakening of supervision of banks under $200 billion playing a role in this affair. But the regulators were on to the problems at Silicon Valley Bank. What appears to have been missing was not recognizing the Silicon Valley Bank was train wreck in the making, but the failure to make adequate interventions.

The Times does serve up one idea:

Officials could ask whether banks with $100 billion to $250 billion in assets should have to hold more capital when the market price of their bond holdings drops — an “unrealized loss.” Such a tweak would most likely require a phase-in period, since it would be a substantial change.

First, this is not such a hot idea because when interest rates are rising, bank stock prices are weak. This is why banks can get into a doom loop: they need more equity precisely at the time no one except Warren Buffett (who is usually able to extract official subsidies) is willing to give it to them. The time to strengthen capital levels are when times are good. Rules like this could well wind up being prejudicial: if a bank was healthy but trying to build up more reserves pre-emptively in a tightening cycle, it could be assumed to be already in trouble.

Second, the regulators had already started dinging Silicon Valley Bank and were giving it more demerits, yet actual punishment was non-existent. Some think, as the Times mentions, that the SVB CEO being on a San Francisco Fed advisory board contributed to the overly deferential treatment. Bear in mind the regional Fed boards have absolutely zero influence over those bodies. They do not supervise regional Fed operations or staff in any way, shape or form.

However, cozy relations at the top could easily make staffers fear that their critical assessment would be watered down or ignored, even before getting to the general pattern in the US of undue deference towards the regulated. This sort of thing has happened, witness the case of New York Fed whistleblower Carmen Segarra, who was fired from the New York Fed for not being willing to weaken her findings about deficiencies at Goldman.

Where are the Benjamin Lawskys, who threatened recidivist money launderer Standard Chartered with revoking its New York banking license?4 Without going down the rabbit hole of the finer points of procedure, if noting else, the Fed has the power to take formal enforcement actions. The New York Times account suggests things were going enough off the rails for the regulator to at least threaten one as of a date certain if Silicon Valley Bank failed to remedy some of its deficiencies. But obviously no serious action was taken.

Now to the other big news sick bank, Credit Suisse. Its collapse reflects the even bigger regulatory failure in Europe, whose post-crisis reforms managed to make ours look good.

Admittedly, Europe has the big misfortune to have universal banks. These are banks that do everything from retail banking to fancy Wall Street wizardry. They are also much bigger in GDP terms in aggregate than US banks because Europe has much smaller bond markets, so bank lending is an ever more important source of funding.

But these institutions grew up from being retail banks and never grew out of it. That means they are typically slow-footed and not well run. If more competent leaders come in, they usually can’t effect much change or like Jospf Ackermann of Deutsche Bank, succeed in “transforming” the bank so as to facilitate executive enrichment.

Europe had undercapitalized banks going into the 2008 crisis and failed to make them do enough in lowering their overall leverage levels. They also failed to undo the pernicious relationship between sovereign debt and bank balance sheets, where weak banks hold the debt of weak countries like Italy, where only the tender ministrations of the ECB keep those bond yields down, which helps these states fund at the expense of having ticking time bombs on bank balance sheets (if the ECB let sovereign bond yields go to market levels, a lot of banks would have big holes in their balance sheets).

So long before this crisis got a good head of steam, Deutsche Bank and the Italian banking system were widely recognized as wobbly. Monte del Pasci was bailed out in 2016. There have been complicated efforts to defuse UniCredit, the biggest, sickest Italian bank. Deutsche Bank, despite having raised nearly $30 billion in equity over time, looked positively green in 2017, with Mr. Market rejecting a turnaound plan.

But as Nick Corbishley has dutifully chronicled, Credit Suisse became the sickest European bank in 2021 due to weak earnings and some impressively bad business calls, most importantly being very exposed to the failed supply chain financier Greensil. Why didn’t the Swiss National Bank act after it took that body blow?

Keeping in mind that both of Switzerland’s behemoths, UBS and Credit Suisse, got in a heap of trouble in the crisis, with UBS being one of the most enthusiastically self-destructive users of CDOs. Not only did they eat a lot of their own bad cooking, but they were a leader in the so-called negative basis trade, which was a spectacular form of looting. The short version is traders bought other people’s CDOs, supposedly insured them with credit default swaps, and then got to book all the expected future profit in the current P&L and get paid bonuses on those fictive profits.

Switzerland, after an enormous rescue of UBS, ordered both big banks to get out of investment banking and go back to being private banks. That resolve to revert to the simple life was undermined by the US going after Swiss banking secrecy, leading sneaky American customers to decamp to “no tell” jurisdictions like Singapore and Mauritius. I am not up to speed on Swiss oversight, but l’affaire Greensil suggests the SNB was letting its big charges walk on the wild side again.

To confirm the debilitated state of Credit Suisse has been well known, some snippets from Nick’s posts:

September 2022 Fast-Shrinking TBTF Giant Credit Suisse Is Living Dangerously:

It was in the Spring of 2021 when Credit Suisse’s current crisis began. And that crisis has revealed glaring flaws in its risk management processes.

As readers may recall, two of the bank’s major clients — the private hedge fund Archegos Capital and the Softbank-backed supply chain finance “disruptor” Greensill — collapsed in the same month (March 2021). By the end of April 2021, Credit Suisse had reported losses of $5.5 billion from its involvement with Archegos. Its losses from its financial menage ? trois with Greensill and its primary backer, Softbank, are still far from clear, as the bank is trying to claw back almost $3 billion of unpaid funds for its clients (more on that later).

October 2022 Credit Suisse is One of 13 Too-Big-to-Fail Banks in Europe, But It Looks Like It Could Be Failing:

Credit Suisse is one of 13 European lenders on the Financial Stability Board’s list of Global Systemically Important Banks (G-SIBs). In other words, it is officially too big to fail, but it is nonetheless precariously close to failing. Yesterday it disclosed a whopping third-quarter loss of $4 billion — more than eight times average estimates of just under $500 million. The loss was largely the result of a reassessment of so-called deferred tax assets (DTA).*

This is Credit Suisse’s fourth quarterly net loss in a row. So far this year, it has posted $5.94 billion of losses. Net revenue, at $3.8 billion, was up marginally on the previous quarter but down 30% from Q3-2021. The value of its asset base has shrunk drastically, from $937 billion in December 2020 to $707 billion today. The group’s common equity Tier 1 ratio has also fallen to 12.6%, well below its target of at least 13.5%.

To right the ship, CS has presented a new strategic overhaul — its third in recent years….

I could give you more of what amount to interim reports from Nick, but you get the drift of the gist.

To keep this post to a manageable length, as most of you know, UBS entered into a shotgun marriage with Credit Suisse over the weekend. The nominal purchase price was close to $3 billion, but watch the shell game. From the Wall Street Journal:

The Swiss government said it would provide more than $9 billion to backstop some losses that UBS may incur by taking over Credit Suisse. The Swiss National Bank also provided more than $100 billion of liquidity to UBS to help facilitate the deal.

UBS and European bank stocks opened down, in a vote of not much confidence, although the bank stocks have pared their losses. Mr. Market appears to have worked out that merging two dogs does not produce one healthy cat.

Central banks are also signaling panic by opening emergency swap lines. This action is aimed at helping banks whose home county is not the US get dollar funding (their home country bank will create home country currency, swap it into dollars, and then lend it to their banks). This suggests that foreign banks are having trouble borrowing dollars, or at least on good enough terms. They would need to borrow dollars to fund dollar positions. Are we to assume that this intervention is occurring because haircuts on Treasuries used in repos have gone up? Informed reader input appreciated. From the Financial Times:

The Federal Reserve and five other leading central banks have taken fresh measures to improve global access to dollar liquidity as financial markets reel from the turmoil hitting the banking sector.

In a joint statement on Sunday, the central banks said that, from tomorrow, they would switch from weekly to daily auctions of dollars in an effort to “ease strains in global funding markets”.

The daily swap lines between the Fed and the European Central Bank, the Bank of England, the Swiss National Bank, the Bank of Canada and the Bank of Japan would run at least until the end of April, the officials said.

Of course, the Fed could have addressed the problem of interest rate increase overshoot directly by cutting interest rates by 50 basis points and making noises that quantitative tightening was on hold for the moment. But panic is too far advanced for that sort of simple intervention to now have much impact.

Finally, back to a main point, that yet more subsidies of banks will simply enable more incompetence and looting absent getting bloody-minded regulators, a prospect that seems vanishingly unlikely.

Elizabeth Warren is again taking up her bully pulpit of calling for more bank reform, but technocratic fixes are inadequate with a culture of timid enforcement. The only remedy in all the years I have read about that might have a real impact quickly creates real skin in the game. It proposed by of all people former Goldmanite, later head of the New York Fed William Dudley.

Dudley recommended putting most of executive and board bonuses in a deferred account, IIRC on a rolling five-year basis. If a bank failed, was merged as part of a regulatory intervention, or wound up getting government support, the deferred bonus pool would be liquidated first, even before shareholder equity. Skin in the game would do a lot more to curb reckless behavior than complex new rules.

Of course, Dudley’s proposal landed like a lead balloon.

Loading…

The post Fed, Central Banks Created The Current Crisis And Are On Course To Making Matters Worse appeared first on Energy News Beat.