[[{“value”:”

Quantitative Tightening shed 44% of Pandemic-QE assets. Fed’s share of the ballooning US national debt dropped to the lowest since 2019.

By Wolf Richter for WOLF STREET.

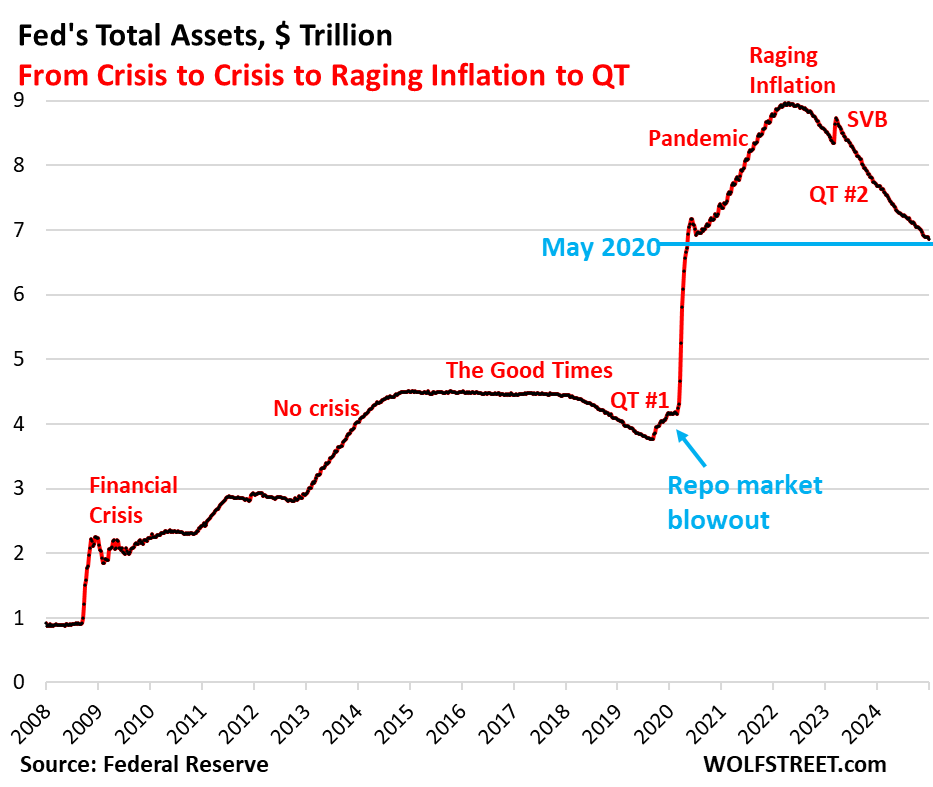

Total assets on the Fed’s balance sheet declined by $43 billion in December, to $6.85 trillion, the lowest since May 2020, according to the Fed’s weekly balance sheet today.

Since the end of QE in April 2022, the Fed has shed $2.11 trillion, or 23.6% of its assets.

In terms of the $4.81 trillion piled on the balance sheet during pandemic QE from March 2020 through April 2022, the Fed has now shed 44% of that.

QT assets by category.

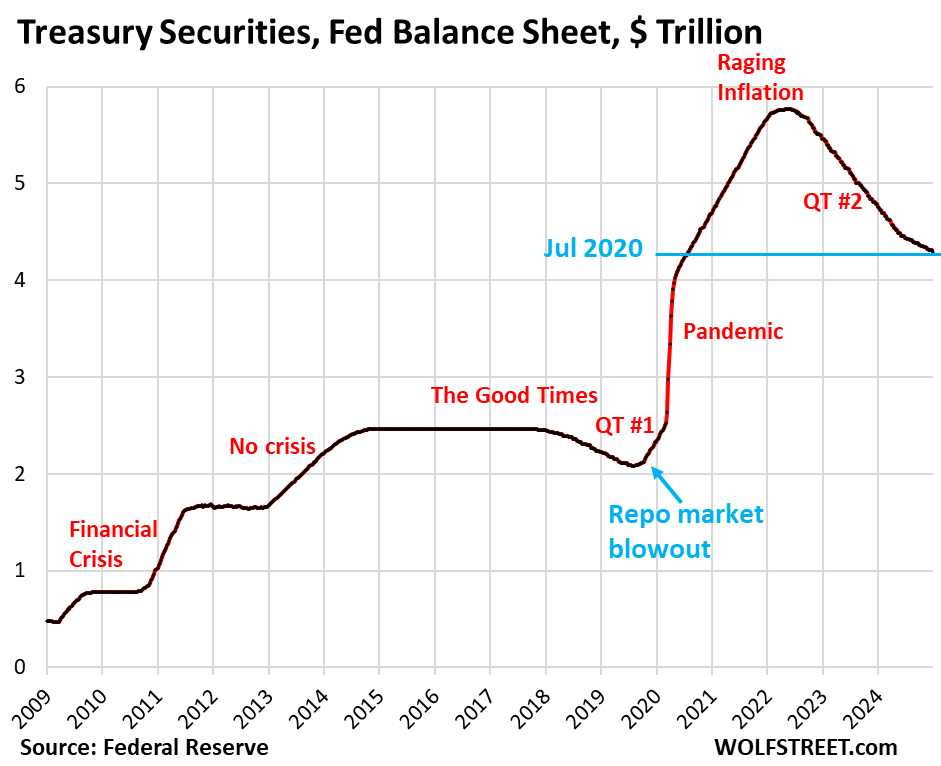

Treasury securities: -$24.5 billion in December, -$1.48 trillion from peak in June 2022, or -26% since the peak, to $4.29 trillion, the lowest since July 2020.

In terms of the $3.27 trillion in Treasuries piled on the balance sheet during pandemic QE, the Fed has now shed 45% of it.

Treasury notes (2- to 10-year) and Treasury bonds (20- & 30-year) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. Since June, the roll-off has been capped at $25 billion per month. About that much rolled off in December, minus the amount of inflation protection the Fed earns on its Treasury Inflation Protected Securities (TIPS) that was added to the principal of the TIPS.

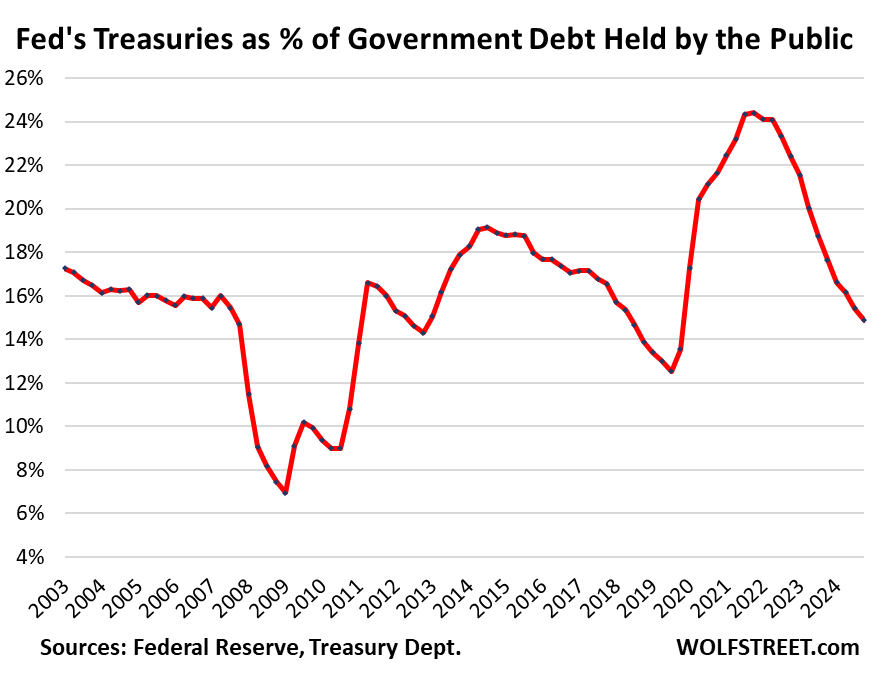

The Fed’s share of the “Debt held by the public” has been declining sharply since mid-2022, as the US national debt has surged at a mindboggling pace, while the Fed started cutting its holdings at the same time. Investors in the US and around the globe have stepped in to buy what the Fed has walked away from.

Of the $36.1 trillion US national debt, $7.30 trillion are held by various federal government pension funds, military pension funds, the Social Security Trust Funds, Medicare Trust Funds, etc.

The remaining $28.87 trillion are “held by the public,” including by the Fed, foreign investors, banks, individuals, etc., and we have laid out these investors by category here.

The Fed’s Treasury holdings of $4.29 trillion amount to 14.9% of the “debt held by the public,” the lowest since Q4 2019.

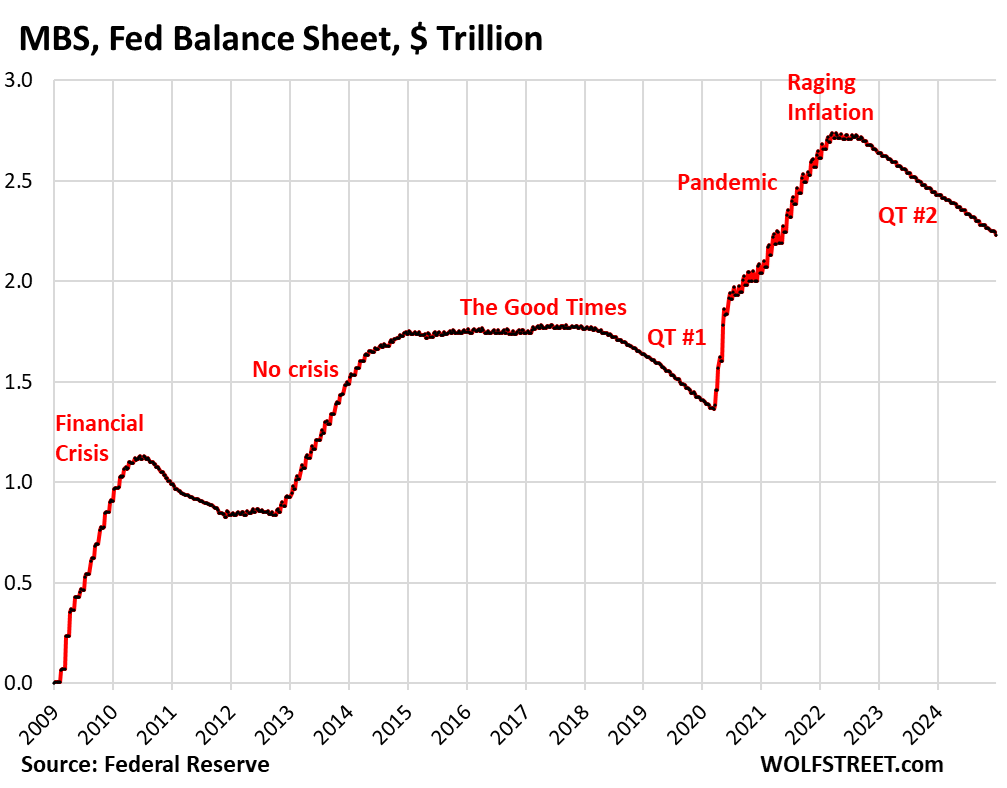

Mortgage-Backed Securities (MBS): -$15.7 billion in November, -$507 billion from the peak, to $2.23 trillion, the lowest since May 2021. The Fed has shed 18.5% of its peak holdings in April 2022.

In terms of the $1.37 trillion in MBS that the Fed added between March 2020 and April 2022, it has shed 37% of it.

MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made. But sales of existing homes in 2024 have plunged to the lowest since 1995 and mortgage refinancing has collapsed, and therefore far fewer mortgages got paid off, and passthrough principal payments to MBS holders, such as the Fed, have become a trickle. As a result, MBS have come off the Fed’s balance sheet at a pace that has been below $20 billion in most months.

There has been some discussion at the Fed, including in October by Dallas Fed President Lorie Logan, about outright selling MBS to speed up the process of getting rid of them, and getting rid of all of the MBS even after QT ends, and replacing them with Treasury securities. But the Fed doesn’t seem to be in a hurry to tackle this topic.

The Fed only holds “agency” MBS that are guaranteed by the government, and is therefore not exposed to losses if borrowers default on mortgages; the taxpayer would pick up those losses, not the Fed.

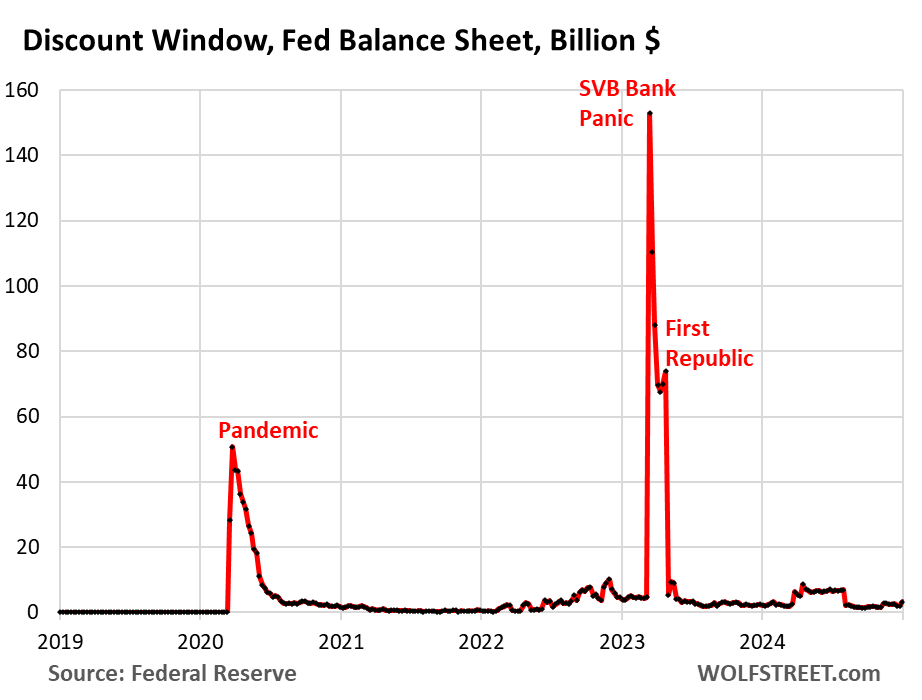

Bank liquidity facilities.

The only two bank liquidity facilities that currently have a balance that’s above zero or near-zero are the Discount Window and the Bank Term Funding Program (BTFP). The other bank liquidity facilities that were heavily used after the SVB collapse are either at zero or near zero:

- Central Bank Liquidity Swaps ($1 billion)

- Repos ($0)

- Loans to the FDIC ($0).

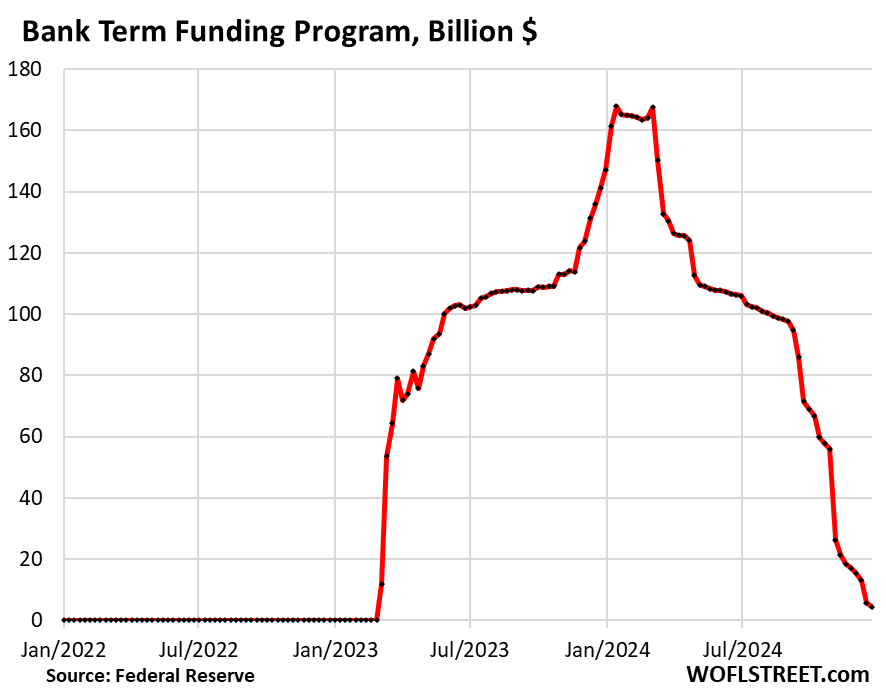

Bank Term Funding Program (BTFP): -$13 billion in December, to $4 billion, -97% from the peak ($168 billion).

The BTFP had a fatal flaw when it was conceived in March 2023 after SVB had failed: Its rate was based on a market rate. When Rate-Cut Mania kicked off in November 2023, market rates plunged even as the Fed’s policy rates were unchanged, including the 5.4% the Fed paid banks on reserves at the time. Some banks then used the BTFP for arbitrage profits, borrowing at the BTFP at a lower market rate and leaving the cash in their reserve account at the Fed to earn 5.4%. This arbitrage caused the BTFP balances to spike to $168 billion.

The Fed shut down the arbitrage in January by changing the rate and decided to let the BTFP expire on March 11, 2024, and no new loans could be taken out since then. Any remaining loans, which had a maximum term of one year, will be paid off by March 11, 2025, and the balance will go to zero.

Discount Window: +$800 million in December, to $3.2 billion. During the bank panic in March 2023, loans had spiked to $153 billion.

The Discount Window is the Fed’s classic liquidity supply to banks. As of the rate cut in December, the Fed charges banks 4.50% in interest on these loans and demands collateral at market value, which is expensive money for banks.

In his efforts to water down the stigma attached to borrowing at the Discount Window, Powell has been exhorting banks to use this facility more often, and practice using it with small-value exercise transactions, and to even get set up to use it, which many banks apparently are not, and to pre-position collateral so that they can use it when they need to.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post Fed Balance Sheet QT: -$43 Billion in December, -$2.11 Trillion from Peak, to $6.85 Trillion. Bank-Panic BTFP Nearly Gone appeared first on Energy News Beat.

“}]]