[[{“value”:”

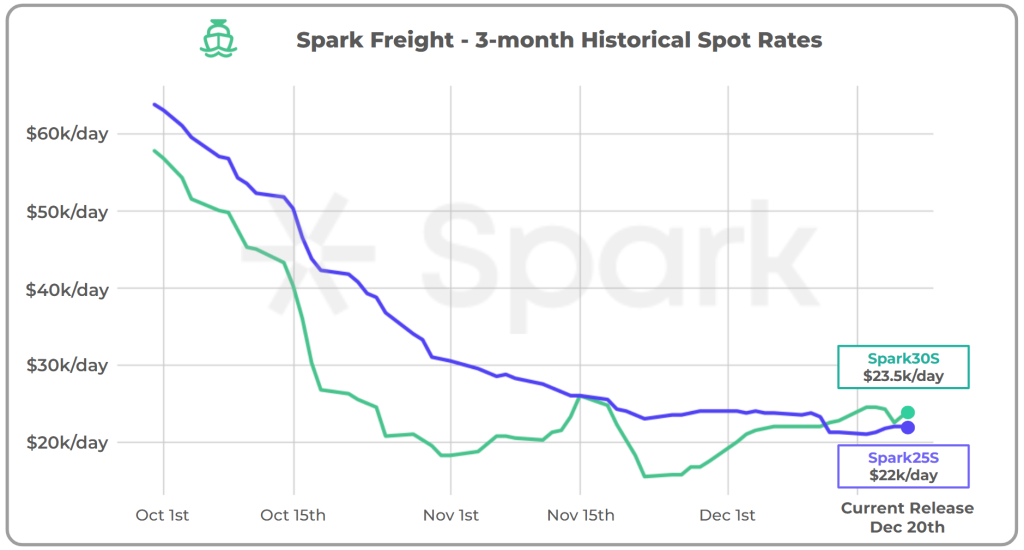

“Spark30S rates rose for a fourth consecutive week, increasing marginally by $750 to $23,500 per day,” Qasim Afghan, Spark’s commercial analyst, told LNG Prime on Friday.

“Q4 2024 is pricing in as the lowest quarter on record for a 174 2 stroke vessel, with Q1 and Q2 2025 currently assessed at even lower levels,” Afghan said.

He said Spark25S Pacific rates rose by $750 to $22,000 per day.

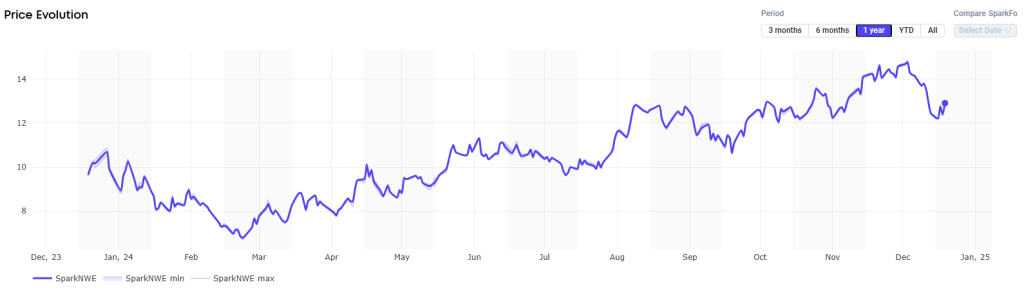

In Europe, the SparkNWE DES LNG was almost flat compared to 12.914 MMBtu last week.

“The SparkNWE DES LNG front month price for January delivery stayed relatively steady at $12.913/MMBtu, reaching a quarterly low at the start of this week at $12.212/MMBtu but experiencing a small recovery since then,” Afghan said.

He said the discount to the TTF narrowed slightly this week to -$0.190/MMBtu.

“The US arb to NE-Asia (via the Cape of Good Hope) for January is still currently closed, narrowing by $0.053 to -$0.313/MMBtu and signaling that US cargos are incentivized to deliver to NW-Europe instead,” Afghan said.

“The US arb to NE-Asia via Panama Canal is much more marginal, pricing in as closed at -$0.077/MMBtu,” he said.

Data by Gas Infrastructure Europe (GIE) shows that volumes in gas storages in the EU continued to decline significantly and were 76.73 percent full on December 18.

Gas storages were 80.16 percent full on December 11, 2024, and 88.20 percent full on December 18, 2023.

In Asia, JKM, the price for LNG cargoes delivered to Northeast Asia in February 2025 settled at $13.460/MMBtu on Thursday.

Last week, JKM for January settled at 14.877/MMBtu on Friday, December 13.

Front-month JKM dropped to 12.765/MMBtu on Monday. It rose to 13.320/MMBtu on Tuesday and dropped to 13.005/MMBtu on Wednesday.

State-run Japan Organization for Metals and Energy Security (JOGMEC) said in a report earlier this week that JKM for last week (December 9–13) fell to mid-$13s on December 13 from high-$14s the previous weekend.

“JKM was on downward trend through the week as high inventories and weak demand in Northeast Asia continued,” JOGMEC said.

Maritime consultancy Drewry said in a report this week that LNG shipping rates are expected to soften further in 2025.

Drewry said 96 LNG carriers are scheduled to be delivered next year, aggravating the oversupply situation.

The firm expects the scrapping of steam turbine carriers to rise next year as these vessels invariably become idle with no re-employment opportunities and act as a ‘buffer’ in the total supply, further limiting any potential growth in rates.

“Considerable scrapping (of about 30-40 carriers) will be required to restore the supply-demand balance and stabilize rates next year,” Drewry said.

According to the consultancy, the additional 42 mtpa of new capacity will be insufficient to balance the fleet growth.

Drewrs said the demand outlook is mixed, varying regionally – a slight recovery is expected in Europe while Asia will remain the primary growth hub.

Meanwhile, how the 2024-25 winter ends will be pivotal for Europe’s LNG demand next year, Drewry said.

We give you energy news and help invest in energy projects too, click here to learn more

Crude Oil, LNG, Jet Fuel price quote

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack

The post Spot LNG rates remain weak appeared first on Energy News Beat.

“}]]